Gobernanza e internacionalización en los resultados de las empresas: Un estudio de caso en Indonesia y Malasia

Governance and internationalisation on firm performance: A case study in Indonesia and Malaysia

Werner R. Murhadi

University of Surabaya (Indonesia)

https://orcid.org/0000-0002-7297-861X

Shiendy S. Setiawan

University of Surabaya (Indonesia)

s130219088@student.ubaya.ac.id

Endang Ernawati

University of Surabaya (Indonesia)

Endangernawati@staff.ubaya.ac.id

RESUMEN

Objetivo: Este estudio pretende determinar el efecto de las prácticas de gobernanza y el grado de internacionalización en las empresas de Indonesia y Malasia. La investigación sobre la gobernanza en Indonesia es interesante debido a su incoherente aplicación de la ley y a la existencia de una propiedad familiar dominante que puede expropiar a los accionistas externos. Diseño y métodos de investigación: Este estudio utiliza una muestra de empresas manufactureras ubicadas en Indonesia y Malasia. El estudio utiliza datos de panel con variables independientes de gobernanza y grado de internacionalización. Resultados: Los resultados muestran que las variables de gobernanza que utilizan el proxy de comisarios independientes, el tamaño del consejo y la presencia de comisarias influyen en los resultados financieros. Al mismo tiempo, la gobernanza como variable sustitutiva de la frecuencia de las reuniones del consejo no afecta a los resultados financieros. El grado de internacionalización arrojó resultados que también afectan a los resultados financieros. Las empresas que entran en el mercado internacional también necesitan una buena gobernanza. Implicaciones y recomendaciones: Implicaciones prácticas, Se espera que los inversores tengan en cuenta los aspectos de gobierno corporativo e internacionalización a la hora de invertir. Como muestran los resultados de la investigación presentados anteriormente, diversas variables, como los comisarios independientes, el tamaño del comisario y el coeficiente de exportación, también afectan a los resultados de la empresa. Se aconseja a los inversores, especialmente en Indonesia, que inviertan en empresas con el número óptimo de comisarios independientes para obtener el máximo rendimiento. Además, se aconseja a los inversores que elijan empresas con el número óptimo de consejos de comisarios para maximizar el rendimiento de la empresa. Contribución y valor añadido: La investigación contribuye utilizando una combinación de cuestiones de gobierno corporativo e internacionalización que pueden beneficiar a la empresa y a la economía nacional.

PALABRAS CLAVE

Gobierno corporativo; internacionalización; tamaño de los consejos; mujeres comisarias; resultados financieros.

ABSTRACT

Objective: This study aims to determine the effect of governance practices and the degree of internationalization on companies in Indonesia and Malaysia. Research on governance in Indonesia is interesting because of its inconsistent law enforcement and the existence of dominant family ownership that can expropriate external shareholders. Research Design & Methods: This study uses a sample of manufacturing companies located in Indonesia and Malaysia. The study uses panel data using independent governance variables and degree of internationalization. Findings: The results showed that governance variables using the proxy of independent commissioners, the board size, and the presence of female commissioners influence financial performance. At the same time, governance as of a proxy for the frequency of board meetings does not affect financial performance. The degree of internationalization found results that also affect financial performance. Companies that enter the international market also need good governance. Implications & Recommendations: Practical implications, Investors are expected to consider corporate governance and internationalization aspects when investing. As the research results presented previously show, several variables, such as independent commissioners, commissioner size, and export ratio, also affect company performance. Investors, especially in Indonesia, are advised to invest in companies with the optimal number of independent commissioners to get maximum returns. In addition, investors are advised to choose companies with the optimal number of boards of commissioners to maximize company performance. Contribution & Value Added: The research contributes by using a combination of corporate governance and internationalization issues that can benefit the company and the national economy.

KEYWORDS

Corporate governance; internationalization; board size; female commissioner; financial performance.

Clasificación JEL: G34, F10, J16.

MSC2010: 62J05.

1. INTRODUCCIÓN

Corporate governance has recently received considerable attention from both business actors and academics. The limitation of shareholders in controlling the company results in the transfer of control to company managers. The separation of ownership and control in the company creates agency conflicts. Managers (agents) often use company resources to maximize their interests and override the interests of shareholders (principals). In addition, there is also asymmetric information because managers as internal parties have better information than shareholders as external parties (Jensen & Meckling, 1976). Therefore, managers’ actions need to be monitored so that the decisions taken align with maximizing shareholder welfare. Better shareholder welfare can be shown by implementing good corporate governance (Mishra & Kapil, 2018). When corporate governance is poor, investors tend to allocate funds to companies with good governance to protect their wealth (Puni & Anlesinya, 2020). Corporate governance has been implemented in Indonesia since 1999 through the establishment the National Committee on Governance Policy (KNKG Indonesia, 2006). However, several problems still need to be addressed in governance in Indonesia (Tanjung, 2020). Utama et al. (2017) said that various studies show that corporate governance practices in Indonesia are relatively worse than in other countries. This is evidenced by the Asian Corporate Governance Association (ACGA) assessment in CG Watch, which ranks Indonesia as the lowest among 12 other Asian countries. In addition, the inconsistent and weak law enforcement in Indonesia has made corporate governance an important issue. Therefore, further improvements are needed in corporate governance in Indonesia, which is expected to reduce conflicts of interest. Corporate governance can address conflicts of interest through monitoring and advisory roles. Not only that, but corporate governance can also reduce asymmetric information conflicts (Al Farooque et al., 2019).

Corporate governance is measured by several measurements, including board independence, board size, board meet, and proportion of female directors. Independent commissioners in Ramadan & Hassan’s (2021) research have no significant effect on ROA or TBQ. Meanwhile, other studies state that independent commissioners have a significant positive effect on ROA and are insignificant to TBQ (Mishra & Kapil, 2018). The cause of the positive influence is that independent commissioners have knowledge and experience from various sources that can affect company performance (Al-Matari, 2020). This is also supported by Shan (2019), who explained that ownership structure and independent commissioners could reduce conflicts of interest between shareholders and company managers.

Meanwhile, Naghavi et al. (2021) state that independent commissioners are insignificant to ROA and have a significant positive effect on TBQ. The board size variable refers to the size of the commissioners, whereas in Indonesia, commissioners have a supervisory and monitoring function. Several studies explain that the size of commissioners is insignificant to ROA and positively significant to TBQ (Ramadan & Hassan, 2021). Meanwhile, other studies show that commissioner size significantly affects company performance, measured by ROA and TBQ variables (Mishra & Kapil, 2018). The cause of positive effect is that a larger commissioner size will present a variety of viewpoints to improve company performance (Ramadan & Hassan, 2021).

Conversely, some studies explain that commissioner size significantly negatively affects ROA and TBQ. The cause of the negative effect is that smaller commissioner sizes are considered more efficient when discussing, coordinating, and communicating, thereby reducing conflicts of interest (Al-Matari, 2020; Naghavi et al., 2021). Smaller commissioner sizes are more efficient in supervision because larger commissioner sizes tend to be more bureaucratic and slow in making decisions (Teti et al., 2017). Furthermore, there is a board meet variable referring to the frequency of commissioner meetings. There are research results that state that the frequency of commissioner meetings is insignificant to ROA and TBQ (Ramadan & Hassan, 2021); meanwhile, other studies state that the frequency of commissioner meetings is insignificant to ROA and has a significant positive effect on TBQ (Mishra & Kapil, 2018). More frequent commissioner meetings improve the quality of supervision and monitoring and reduce information asymmetry, thereby improving company performance (Ramadan & Hassan, 2021). However, the more frequent frequency of commissioner meetings can signal that the company’s performance is in trouble (Malik & Makhdoom, 2016). In addition, the frequency of meetings is also associated with administrative costs in the form of high information processing and preparation, which can reduce company performance (Queiri et al., 2021; Ntim et al., 2017). The presence of women on supervisory boards has also attracted the attention of many researchers. The proportion of female directors or female commissioners in research shows that the proportion of female commissioners has a significant positive effect on ROA and is insignificant to TBQ (Naghavi et al., 2021). The cause of the positive influence is that female commissioners play a role in good corporate governance practices because women tend to be more careful. In addition, female commissioners are more diligent in observing and demanding more frequent audit efforts to improve company performance (Gunawan et al., 2019). Meanwhile, a different study said that the proportion of female commissioners had an insignificant effect on ROA and TBQ (Ramadan & Hassan, 2021).

In addition to focusing on governance, this research also considers the degree of internationalization. The degree of Internationalisation refers to the ratio of exports to revenue. In the era of globalization, companies will have the opportunity to earn revenue abroad. However, involvement in foreign markets takes work. Companies can start with a simple scale from exports to a more complex scale by opening operations abroad. This, of course, also requires good corporate governance before stepping into the international market. Chou et al. (2021) show that the export ratio significantly positively affects ROA. The reason for the positive effect is that the level of internationalization can help develop corporate governance with international standards. In addition, companies can gain knowledge, innovation, and risk diversification (Contractor et al., 2003). Several dimensions of internationalization beyond the export ratio affect governance: Foreign Direct Investments (FDI) and cross-border mergers. By introducing modern governance practices, advanced technologies, and global best practices, FDI significantly impacts governance quality, firm performance, and risk management. FDI enhances governance quality through institutional upgrading, board composition, and transparency. It improves firm performance by transferring technology, expertise, and access to global markets while optimizing resource allocation. Additionally, FDI mitigates risk through diversification, risk sharing, and improved corporate governance, enabling access to international capital markets. Meanwhile, Cross-border mergers significantly impact governance quality, firm performance, and risk management by integrating diverse governance systems, sharing expertise and resources, and expanding market reach. They enhance governance quality through combined board expertise, improved transparency, and regulatory compliance. Firm performance benefits from synergies, economies of scale, and access to new markets. However, cross-border mergers also introduce risks, including cultural and integration challenges, regulatory complexities, and exposure to global market volatility, necessitating robust risk management strategies. This study uses the export ratio proxy, considering that it is adjusted to the characteristics of Indonesia and Malaysia, which dominate the export ratio rather than foreign direct investment or cross-border mergers.

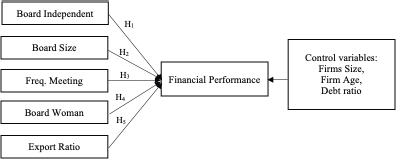

The problems in this study are as follows: (1) Do independent commissioners have a positive influence on the performance? (2) Does the size of the board of commissioners have a negative influence on the performance? (3) Does the frequency of commissioners’ meetings have a negative influence on the performance? (4) Does the proportion of female commissioners have a positive influence on the performance? (5) Does the export ratio have a positive influence on the performance?

2. LITERATURE REVIEW

In addition to focusing on governance, this research also considers the degree of internationalization. The degree of Internationalization refers to the ratio of exports to revenue. In the era of globalization, companies will have the opportunity to earn revenue abroad. However, involvement in foreign markets takes work. Companies can start with a simple scale from exports to a more complex scale by opening operations abroad. This, of course, also requires good corporate governance before stepping into the international market. Chou et al. (2021) show that the export ratio significantly positively affects ROA. The reason for the positive effect is that the level of internationalization can help develop corporate governance with international standards. In addition, companies can gain.

According to Jensen and Meckling (1976), agency theory is a contractual relationship where principals (shareholders) delegate authority to agents (managers) to manage the company to maximize shareholder welfare. This contractual relationship creates agency conflicts, such as interest differences, information asymmetry, and conflicts between majority and minority shareholders. Hanafi et al. (2018) say separating ownership and control roles creates problems between shareholders and managers. In addition, Ramadan & Hassan (2021) say that agents often sacrifice the interests of the principal in order to maximize their benefits, resulting in a conflict of interest. There is also information asymmetry because agents get more accurate information about the company’s condition than the principal (Ain et al., 2021). According to Ramadan & Hassan (2021), agency problems also occur between majority and minority shareholders. This is because majority shareholders often act arbitrarily in exercising control and sacrificing the interests of minority shareholders. The existence of the principal’s distrust of the agent raises agency costs for the company. The company incurs agency costs to overcome differences in the interests of principals and agents. Shan (2019) said that agency costs arise due to supervisory activities carried out by the principal against the agent to protect the interests of the principal.

Corporate governance aims to ensure that managers behave ethically in making decisions to maximize shareholder welfare (Queiri et al., 2021). Corporate governance can increase investor confidence and company capital (Mishra & Kapil, 2018). Good corporate governance can also reduce investment risk and guarantee investment returns (Murhadi et al., 2021). Good corporate governance depends on whether or not shareholders can control managers to maximize firm value (Erena et al., 2021).

Some governance measures to consider good corporate governance are board Structure, which is CEO Duality, Board Size, Board Independence Ratio, Board Meeting Frequency, and Board Diversity. However, in this study, CEO Duality was not measured due to differences in the board system in Indonesia and the USA, so this study only used Board Size, Board Independence Ratio, Board Meeting Frequency, and Board Diversity. This study also does not include elements of Ownership Structure such as Managerial Ownership, given the tiny proportion of managerial ownership in companies in Indonesia.

Independent commissioners positively affect company performance, especially when measured by ROA (Mishra & Kapil, 2018). Agency theory explains that independent commissioners perform better supervisory actions because of the incentive to improve their reputation (Kao et al., 2019). In addition, more independent commissioners can minimize collusion and takeover of shareholder wealth by top management, thereby reducing agency costs (Kao et al., 2019). Agency theory also explains that independent commissioners tend to protect shareholders from risky decisions made by managers (Al-said, 2021). Therefore, independent commissioners are considered to make managers more active and reduce conflicts of interest, increasing company performance. Independent commissioners positively affect company performance, especially when measured by TBQ (Naghavi et al., 2021). Based on this explanation, the following hypothesis is developed:

H1. Independent commissioners have a positive effect on firm performance.

Board size hurts firm performance, whether measured on an accounting or market basis (Naghavi et al., 2021; Lipton and Lorsch, 1992). The reason is that the larger the size of the board is considered to cause the expression of ideas and opinions to be difficult due to time constraints and allow free-riding. In addition, a larger board size is considered to cause difficulties in coordination. It needs to be unified between its members because in making decisions, it must reach an agreement of 1 vote, so this can interfere with company performance.

H2. Board size has a negative effect on company performance.

The frequency of board meetings has a negative effect on company performance, especially when measured on an accounting basis (Queiri et al., 2021). Board meetings can be used to make strategic decisions and discuss management behavior and performance (Mishra & Kapil, 2018). An increase in board meetings indicates a problem requiring immediate attention and improvement (Al Farooque et al., 2019). In addition, the high frequency of meetings also needs to be supported by high administrative costs, increasing company costs (Hanh et al., 2018). Moreover, coupled with the existing culture in Indonesia and eastern countries that tend to discuss other matters outside the set agenda. From this thought, the following hypothesis was developed:

H3. The frequency of board meetings has a negative effect on company performance.

The existence of a female commissioner has attracted current research. Women’s characteristics will be able to balance the supervision carried out by male commissioners. The proportion of female commissioners positively affects firm performance, especially when measured on an accounting basis (Ramadan & Hassan, 2021; Naghaviet al., 2021). Different studies show that gender diversity provides better oversight because women are considered to ask more questions, thereby reducing agency problems (Ain et al., 2021). In addition, gender diversity on the board of commissioners leads to an increase in the number of viewpoints, so monitoring and evaluating decisions is more significant. Therefore, having women serving on the board of commissioners can improve company performance through better monitoring.

H4. The proportion of female commissioners has a positive effect on company performance.

This study also includes the degree of internationalization, which along with the recovery from the Covid 19 pandemic, has encouraged many countries to re-open their borders. The export ratio positively affects firm performance, especially when measured on an accounting basis. The degree of internationalization can help develop corporate governance with international standards (Chou et al., 2021). New geographic markets will expand the consumer base and increase the company’s sales volume (Pacheco, 2019). In addition, internationalization leads to greater market access for the firm, allowing it to produce cheaper inputs. Therefore, a high export ratio can improve firm performance.

H5. The export ratio has a positive effect on firm performance.

From the hypothesis developed above, the research model to be tested appears in Figure 1.

3. METHODS

This study uses a sample of companies incorporated in the manufacturing sector listed on the Indonesia Stock Exchange and Malaysia Stock Exchange. The country selection was based on the corporate governance score of the Asian Corporate Governance Association (ACGA). Malaysia ranked second with the highest corporate governance score in ASEAN, while Indonesia obtained the lowest. Indonesia is weaker than Malaysia due to family ownership, where the company tends to be expropriated. The final sample that met the criteria was 375 years of observation for Indonesia and 445 years of observation for companies in Malaysia. The dependent variable used is firm performance in (FP) the form of ROA and TBQ. The independent variables used consist of 5: independent commissioners (IC), commissioner size (BS), frequency of commissioner meetings (FM), the proportion of female commissioners (PF), and export ratio (ER).

Independent commissioners are measured using the percentage of independent commissioners to total commissioners. The total number of commissioners in the company measures the size of the board of commissioners. The frequency of commissioner meetings is the number of meetings attended by the board of commissioners. Female commissioners are measured by the percentage of female commissioners to total commissioners. The export ratio is measured using the percentage of export value to total sales in a year. The use of the ratio of export to sales takes into consideration that most companies in Indonesia and Malaysia are export-oriented. The majority of companies do not open factories abroad as multinational corporations. Only a few companies in Indonesia and Malaysia make foreign direct investments as multinational corporations. Based on these arguments, most companies still do mode entry abroad in the form of exports, so the proxy for measuring internationalization uses the export-to-sales ratio.

The control variables used consist of 3 variables: firm size, firm age, and leverage. Firm size is measured using the natural logarithm of total assets, firm age is measured by subtracting the current year from the year of establishment, and leverage uses the debt ratio. The data used in this research is panel data regression, so it must follow the panel data testing requirements. Testing is done to determine whether the model to be interpreted is a common, fixed, or random model.

Common Effect Model

(1)

Fixed Effect Model

(2)

Random Effect Model

(3)

To determine which model to interpret, the Chow and Hausman tests were conducted.

3. FINDING and DISCUSSION

Table 1 shows the correlation of variables for companies in Indonesia. From Table 1, there is no multicollinearity in the variables for companies in Indonesia.

Table 1. Correlation between variables in Indonesia

|

Board Independent |

Board Size |

Freq. Meeting |

Board Woman |

Export Ratio |

Firm Size |

Firm Age |

Debt Ratio |

|

|---|---|---|---|---|---|---|---|---|

|

Board Independent |

1.00 |

–0.06 |

–0.12 |

–0.01 |

–0.13 |

0.19 |

0.23 |

0.06 |

|

Board Size |

–0.06 |

1.00 |

–0.13 |

–0.16 |

–0.10 |

0.46 |

0.21 |

0.03 |

|

Freq. Meeting |

–0.12 |

–0.13 |

1.00 |

0.01 |

0.01 |

–0.08 |

0.07 |

0.18 |

|

Board Woman |

–0.01 |

0.16 |

0.01 |

1.00 |

0.01 |

–0.12 |

–0.03 |

0.17 |

|

Export Ratio |

–0.13 |

–0.10 |

0.01 |

0.01 |

1.00 |

0.04 |

–0.27 |

0.24 |

|

Firm Size |

0.19 |

0.46 |

–0.08 |

–0.12 |

0.04 |

1.00 |

0.22 |

0.14 |

|

Firm Age |

0.23 |

0.21 |

0.07 |

–0.03 |

–0.27 |

0.22 |

1.00 |

0.04 |

|

Debt Ratio |

0.06 |

0.03 |

0.18 |

0.17 |

0.24 |

0.14 |

0.04 |

1.00 |

Table 2 shows the correlation of variables for Malaysian firms. Table 3 also shows no multicollinearity between variables in Malaysian companies.

Table 2. Correlation between variables in Malaysia

|

Board Independent |

Board Size |

Freq. Meeting |

Board Woman |

Export Ratio |

Firm Size |

Firm Age |

Debt Ratio |

|

|---|---|---|---|---|---|---|---|---|

|

Board Independent |

1.00 |

–0.61 |

–0.09 |

–0.01 |

–0.03 |

–0.21 |

–0.10 |

0.13 |

|

Board Size |

–0.61 |

1.00 |

0.20 |

–0.02 |

–0.05 |

0.32 |

0.17 |

–0.00 |

|

Freq. Meeting |

–0.09 |

0.20 |

1.00 |

–0.07 |

–0.10 |

0.21 |

0.04 |

0.09 |

|

Board Woman |

–0.01 |

–0.02 |

–0.07 |

1.00 |

0.20 |

0.05 |

–0.13 |

0.06 |

|

Export Ratio |

–0.03 |

–0.05 |

–0.10 |

0.20 |

1.00 |

0.00 |

–0.17 |

–0.10 |

|

Firm Size |

–0.21 |

0.32 |

0.21 |

0.05 |

0.00 |

1.00 |

0.33 |

0.07 |

|

Firm Age |

–0.10 |

0.17 |

0.04 |

–0.13 |

–0.17 |

0.33 |

1.00 |

0.13 |

|

Debt Ratio |

0.13 |

–0.00 |

0.09 |

0.06 |

–0.10 |

0.07 |

0.13 |

1.00 |

Using panel data requires testing to determine the best model between common, fixed, and random effects. After conducting the Chow and Hausmann tests, the best model used the fixed effect in Indonesia and Malaysia.

In Table 3, independent boards positively affect ROA in Indonesia and Malaysia. The more independent boards, the better at supervising the directors (Gunawan et al., 2019). In addition, independent commissioners who supervise effectively can reduce agency problems (Fuzi et al., 2016). Companies with many independent boards of commissioners can improve company performance because there are no personal interests (Ahmadi et al., 2018). Independent boards can protect shareholders from managers’ risky decisions (Al-said, 2021). Testing the board independency variable shows consistent results in both Indonesia and Malaysia.

Table 3 Regression results with dependent variable ROA for both Indonesia and Malaysia.

|

Variable |

Indonesia |

Malaysia |

||

|---|---|---|---|---|

|

Coef. Regression |

t-stat |

Coef. Regression |

t-stat |

|

|

Constant |

–1.671 |

–6.05*** |

–2.208 |

–9.08*** |

|

Board Independent |

0.057 |

5.36*** |

0.024 |

2.62* |

|

Board Size |

–0.005 |

–7.65*** |

0.009 |

2.89** |

|

Freq. Meeting |

–0.000 |

–0.76 |

–0.000 |

–0.39 |

|

Board Woman |

–0.037 |

–2.82* |

–0.026 |

–2.54* |

|

Export Ratio |

–0.040 |

–4.54** |

0.000 |

0.03 |

|

Firm Size |

0.076 |

6.17*** |

0.087 |

8.42*** |

|

Firm Age |

–0.007 |

–4.28** |

–0.004 |

–3.04** |

|

Debt Ratio |

–0.263 |

–16.83*** |

–0.236 |

–11.09*** |

|

R-Squared |

0.90 |

0.81 |

||

|

Adj. R. Squared |

0.88 |

0.76 |

||

|

F-Stat |

33.19*** |

15.33*** |

||

Note: * significant at 10 %; ** significant at 5 %; *** significant at 1 %

The Board Size variable has a significant negative effect on ROA for the case of Indonesia and a significant positive for the case of Malaysia. The results of research in Indonesia that found negative results were because smaller board sizes tend to make all members contribute fully, know each other well, and hold discussions effectively to reach an agreement (Naghavi et al., 2021; Lipton & Lorsch, 1992; Kao et al., 2019). The finding of negative results in Indonesia can be explained that a smaller number of commissioners will be more effective in coordinating and avoiding free riding (Lukito et al., 2024). Regarding the difference in the significance of the Commissioner Size variable, it can be explained because most of the companies listed in Indonesia are family companies, so the role of the family in controlling the company is very large. In family companies, often family members will be appointed to the board of directors and commissioners. The stronger the family involvement, the potential for differences in interests that cause agency conflicts will arise. While the results in Malaysia, which show significant positive results, align with research conducted by Mishra & Kapil (2018) and Queiri et al. (2021). This result is because a larger board size will present a variety of viewpoints from the board to improve company performance (Ramadan & Hassan, 2021). The number of boards indicates more diverse competencies and better supervision of top management to reduce asymmetric information (Puni & Anlesinya, 2020).

The Frequency of board Meetings variable shows insignificant results in Indonesian and Malaysian cases. The Frequency of board meetings is insignificant to company performance because the emphasis is on the quality of meetings rather than the Frequency of meetings (Al-Matari, 2020; Ramadan & Hassan, 2021). In addition, the board is not allowed to interfere in company decision-making (Cahyadi et al., 2018). The number of meetings to be held is also often scheduled each year. Thus, these things explain the insignificant relationship between the number of commissioner meetings and company performance. Testing the frequency of meeting variable shows consistent results in both Indonesia and Malaysia.

The variable Proportion of Females on board significantly negatively affects both cases in Indonesia and Malaysia. This negative is because the presence of female commissioners can increase the number of conflicts, increase the need for cooperation, and reduce the quality of communication (Pletzer et al., 2015; Satria et al., 2020; Ahmad et al., 2020).. Another explanation for these negative results is that women tend to have more careful and detailed characteristics (Murhadi et al., 2021; Gunawan et al. (2019), which gives rise to many critical opinions and questions that will take time, especially when the company is needed to react quickly (Smith et al., 2006). The negative effect of the proportion of female commissioners can be explained by family companies dominating companies listed in Indonesia and Malaysia so that families will control most companies. In addition, the presence of female commissioners is more likely to be related to family relationships than to actual competence (Murhadi et al., 2021). Testing the proportion of female variables shows consistent results in Indonesia and Malaysia.

The export ratio variable shows a significant negative result on ROA for the case of Indonesia and does not affect the case of Malaysia. According to research conducted by Huang & Marciano (2020) and Lu & Beamish (2001), the export ratio significantly negatively affects ROA. This is because exports can cause an increase in coordination costs, control of export activities, labor wages, and transportation costs due to the increasing geographical distance from foreign markets that the company has entered (Fryges & Wagner, 2010). The results of research conducted by Chadys et al. (2018) show that the export ratio significantly negatively affects performance due to competition with other companies in the market to be entered, ineffective communication and coordination, and the risk of currency exchange rate fluctuations. Meanwhile, the degree of internationalization, as measured by the export ratio, does not affect the performance of companies in Malaysia. This insignificant relationship can be explained through research conducted by Singla & George (2013) and Vithessonthi & Racela (2015), which say that export activities for companies in emerging markets are less desirable because the domestic market provides high growth opportunities (Singla & George, 2013).

Table 4. The regression results with the dependent variable Tobin’s Q for Indonesia and Malaysia.

|

Variable |

Indonesia |

Malaysia |

||

|---|---|---|---|---|

|

Coef. Regression |

t-stat |

Coef. Regression |

t-stat |

|

|

Constant |

10.479 |

8.23*** |

1.251 |

1.28 |

|

Board Independent |

–0.259 |

–2.80** |

–0.184 |

–0.81 |

|

Board Size |

–0.023 |

–2.15* |

0.017 |

0.58 |

|

Freq. Meeting |

–0.007 |

–1.75 |

–0.007 |

–0.32 |

|

Board Woman |

–0.689 |

–4.19** |

–0.361 |

–1.93* |

|

Export Ratio |

–0.139 |

–2.26* |

0.291 |

2.19** |

|

Firm Size |

–0.254 |

–5.81*** |

–0.002 |

–0.06 |

|

Firm Age |

–0.026 |

–9.68*** |

–0.006 |

–2.16** |

|

Debt Ratio |

0.422 |

5.24*** |

0.450 |

1.97** |

|

R-Squared |

0.93 |

0.81 |

||

|

Adj. R. Squared |

0.90 |

0.76 |

||

|

F-Stat |

43.97*** |

15.33*** |

||

Note: * significant at 10 %; ** significant at 5 %; *** significant at 1 %

Table 4 shows that independent commissioners hurt Tobin’s Q for companies in Indonesia and are not significant for companies in Malaysia. The negative results in Indonesia can be explained by the fact that independent commissioners need to supervise management effectively, so they have been unable to improve company performance. The existence of independent commissioners who need to be more experienced and knowledgeable regarding a company’s objectives will also be a burden to the company. Other studies support negative results, considering that if there is a smaller number of independent commissioners, the activities of supervising company management can be more coordinated, thereby improving company performance (Bhagat & Bolton, 2019). Some other theoretical reasons that may explain this are: Independent commissioners might not possess sufficient knowledge about the company and its operations, hindering their ability to make informed decisions. This lack of understanding can lead to ineffective governance. Independent commissioners may not fully comprehend the company’s intricacies, causing them to make decisions detrimental to Tobin’s Q. This could be exacerbated by inadequate training or insufficient industry experience. Independent commissioners may prioritize shareholder interests over the company’s long-term goals, leading to decisions that negatively impact Tobin’s Q. This conflict of interest can result in suboptimal performance. Meanwhile, in the case of Malaysia, the results were found to be insignificant. This study’s results align with research conducted by Mishra & Kapil (2018). The research results conducted by Al-Saidi (2021) also say that independent commissioners have an insignificant effect on company performance, as represented by TBQ. For the market, independent commissioners fail to represent shareholders’ interests well (Octosiva et al., 2018). In addition, there is a possibility that companies appoint independent commissioners not based on their abilities but only to fulfill regulations so that independent commissioners do not affect company performance (Octosiva et al., 2018). Divergent regulatory environments between Indonesia and Malaysia might contribute to the varying impact of independent commissioners on Tobin’s Q. Malaysia’s governance framework better supports independent commissioners’ effectiveness. Another explanation is that Company-specific factors, such as ownership structure, board composition, and industry dynamics, can influence the relationship between independent commissioners and Tobin’s Q. These factors may differ significantly between Indonesian and Malaysian companies.

The board size variable has a significant negative effect on Tobin’s Q in Indonesia and is not significant in Malaysia. This negative is because fewer commissioners will be more effective (Jensen, 1993; Dharmadasa et al., 2014)). In addition, a larger commissioner size makes it challenging to coordinate and free-riding (Lipton & Lorsch, 1992). Meanwhile, for Malaysia, commissioner size has an insignificant effect on firm performance represented by TBQ. For the market, commissioner size cannot improve firm performance. This result is because commissioners with skills and knowledge are more important in influencing company performance than the number of commissioners. Alnasser (2012) also explains that there is no recommendation for the number of commissioners because it is recommended that commissioners participate proactively, make effective decisions and perform all their obligations. Commissioners should be selected based on skills, expertise, experience, and integrity to improve professionalism and qualifications (Nasir & Hashim, 2020). The difference in the significance of the Commissioner Size variable can be explained by the fact that most of the companies listed in Indonesia are family companies, so the family’s role in controlling the company is enormous. Family members will often be appointed to the board of directors and commissioners in family companies. The stronger the family involvement, the potential for differences in interests that cause agency conflicts to arise. This family ownership can be a factor that explains the significant adverse effect on company performance in Indonesia.

Cultural and institutional contexts such as family ownership in Indonesia interact with corporate governance and affect firm performance in several ways. Family ownership can increase cohesion and trust but can also lead to conflicts of interest, unprofessional decision-making, and lack of transparency. In addition, local institutions such as regulations and social norms also influence corporate governance. Cultural and institutional contexts affect firm performance in various ways, such as cultural values that influence decision-making, ownership structures that affect governance, and regulations that affect operations. For example, the collectivist culture in Indonesia encourages collective decisions, while the individualist culture encourages independent decisions. In addition, institutions such as laws and regulations also influence firm performance by setting limits and opportunities. These contexts interact and shape firm performance, both positively and negatively.

The Commissioner Meeting Frequency variable shows consistent results in testing the dependent variable ROA and Tobins Q, where the results show insignificant in both cases in Indonesia and Malaysia. This study’s results align with research conducted by Ramadan and Hassan (2021), which states that the number of commissioner meetings is not significant to company performance. This is an insignificant result because the emphasis is on the quality of meetings rather than the frequency of meetings (Al-Matari, 2020). In addition, the board of commissioners is not allowed to interfere in company decision-making (Cahyadi et al., 2018). The number of meetings to be held is also often scheduled each year. Thus, these things explain the insignificant relationship between the number of commissioner meetings and company performance.

Consistent results were also obtained on the proportion of female commissioners, where significant negative results were found on ROA and Tobins Q for both companies in Indonesia and Malaysia. This negative result is because women tend to have more meticulous and detailed characteristics (Murhadi et al., 2021), resulting in many critical opinions and questions that will take time, especially if the company is required to react quickly (Smith et al., 2006).

Similarly, the export ratio variable for Indonesia consistently provides significant negative results for both ROA and Tobins Q dependent variables. This negative result is because if the company enters foreign markets, there will be competition with other companies in the market it wants to enter. This result requires effective communication and coordination and the risk of currency exchange rate fluctuations when opening foreign markets. At the same time, Malaysia found insignificant results of the influence of the degree of internationalization on ROA and Tobins Q.

4. CONCLUSION

The research results on Independent Commissioners in Indonesia show that independent commissioners have a significant positive effect on the ROA variable and a significant adverse effect on the TBQ variable. This result means that more independent commissioners will improve company performance when viewed from the accounting side but will reduce company performance from the market side. The results of the Commissioner Size study in Indonesia show that the commissioner size variable significantly negatively affects the ROA and TBQ variables. The research results on the Frequency of Commissioners’ Meetings in Indonesia show that the frequency of commissioners’ meetings has an insignificant positive effect on the ROA variable and an insignificant negative effect on the TBQ variable. The research results on the proportion of female commissioners in Indonesia show that the variable proportion of female commissioners significantly negatively affects ROA and TBQ. The results of the Export Ratio study in Indonesia show that the export ratio variable has a significant negative effect on ROA and TBQ. The study results for Malaysia found that board women negatively affect the performance of both RoA and Q, and meeting frequency does not affect performance. Meanwhile, independent board and board size significantly affect RoA but do not significantly affect Q. In contrast, the export ratio does not affect RoA but significantly positively affects Q.

Practical implications: Investors are expected to consider corporate governance and internationalization aspects when investing. As the research results presented previously show, several variables, such as independent commissioners, commissioner size, and export ratio, also affect company performance. Investors, especially in Indonesia, are advised to invest in companies with the optimal number of independent commissioners to get maximum returns. In addition, investors are advised to choose companies with the optimal number of boards of commissioners to maximize company performance. Investors, especially in Malaysia, are advised to invest in companies with an optimal number of independent commissioners and a high export ratio. Another implication for the company is that the results of this study can be taken into consideration to improve corporate governance to improve company performance by paying attention to aspects related to the board of commissioners, especially regarding the number of independent commissioners and the number of commissioners. For companies, especially in Indonesia, it is recommended to increase the number of independent commissioners until they reach the optimal number and the optimal number of boards of commissioners so that company performance is maximized. For companies, especially in Malaysia, it can increase the number of independent commissioners to reach the optimal number and high export ratio so that company performance increases.

This study has several limitations: (1) The research period used; (2) The research object only uses manufacturing companies listed on the Indonesia Stock Exchange and Bursa Malaysia; (3) There are insignificant results; (4) There are other variables outside the variables in this study that can be investigated regarding their influence on company performance. Therefore, it is hoped that future researchers can expand the period and object of research to obtain more accurate and comprehensive research results and add variables that have yet to be previously studied. Future research is also expected to expand the others sector to strengthen the generalization of research results. Future research is also expected to use the MSCI index, although not all companies listed on the Indonesian or Malaysian stock exchanges are included in the MSCI Index. For example, only 20 companies in Indonesia are included in the MSCI Index, while Malaysia only includes the large and mid-cap segments of the Malaysian market.

REFERENCES

, , , & (2020). Women directors and firm performance: Malaysian evidence post policy announcement. Journal of Economic and Administrative Sciences, 36 (2), 96– 109. https://doi.org/10.1108/JEAS-04-2017-0022

, , & (2018). Chief Executive Officer attributes, board structures, gender diversity and firm performance among French CAC 40 listed firms. Research in International Business and Finance, 44, 218–226. https://doi.org/10.1016/j.ribaf.2017.07.083

, , , , & (2021). Female directors and agency costs: evidence from Chinese listed firms. International Journal of Emerging Markets, 16 (8), 1604–1633. https://doi.org/10.1108/IJOEM-10-2019-0818

(2020). Do characteristics of the board of directors and top executives have an effect on corporate performance among the financial sector? Evidence using stock. Corporate Governance (Bingley), 20 (1), 16– 43. https://doi.org/10.1108/CG-11-2018-0358

(2021). Board independence and firm performance: evidence from Kuwait. International Journal of Law and Management, 63 (2), 251–262. https://doi.org/10.1108/IJLMA-06-2019-0145

, , & (2019). Board, audit committee, ownership and financial performance–emerging trends from Thailand. Pacific Accounting Review, 32 (1), 54–81. https://doi.org/10.1108/PAR-10- 2018-0079

(2012). What has changed? The development of corporate governance in Malaysia. Journal of Risk Finance, 13 (3), 269–276. https://doi.org/10.1108/15265941211229271

, , & (2012). The role of board structure as an internal control mechanism in non-listed firms, Innova Ciencia 4 (2), 29–43.

, & (2019). Corporate governance and firm performance: The sequel. Journal of Corporate Finance, 58, 142–168. https://doi.org/10.1016/j.jcorpfin.2019.04.006

, , & (2018). Pengaruh Profitabilitas, Dewan Komisaris, Komisaris Independen dan Risiko Idiosinkratis terhadap Dividend Payout Ratio, Jurnal Economia, 14 (1), 99. https://doi.org/10.21831/economia.v14i1.19404

, , & (2018). Pengaruh Internasionalisasi, Afiliasi Bisnis, dan Research & Development Terhadap Kinerja Perusahaan Manufaktur di Indonesia. Jurnal Siasat Bisnis, 22 (1), 62–75. https://doi.org/10.20885/jsb.vol22.iss1.art4

, , , & (2021). What is the impact of corporate governance on the food industry at different thresholds of internationalization? A review. Agricultural Economics (Czech Republic), 67(1), 21–32. https://doi.org/10.17221/272/2020-AGRICECON

, , & (2003). A three-stage theory of international expansion: The link between multinationality and performance in the service sector. Journal of International Business Studies, 34 (1), 5–18. https://doi.org/10.1057/palgrave.jibs.8400003

, , & (2014). Corporate Governance and Firm Performance: Evidence from Sri Lanka. Journal of Finance and Bank Management, 21 (1), 7–31. https://doi.org/10.15640/jfbm.v3n1a16

, , & (2021). Corporate governance mechanisms and firm performance: empirical evidence from medium and large-scale manufacturing firms in Ethiopia. Corporate Governance (Bingley), 22 (2), 213–242. https://doi.org/10.1108/CG-11-2020-0527

, & (2010). Exports and profitability: First evidence for German manufacturing firms. World Economy, 33 (3), 399–423. https://doi.org/10.1111/j.1467-9701.2010.01261.x

, , & (2016). Board Independence and Firm Performance. Procedia Economics and Finance, 37 (16), 460–465. https://doi.org/10.1016/s2212-5671(16)30152-6

, , & (2019). A study on the effects of good corporate governance – gender diversity on the company performance. Advances in Social Science, Education and Humanities Research, 308, 32–25. https://doi.org/10.2991/insyma-19.2019.9

, , & (2018). Ownership structure and firm performance: evidence from the subprime crisis period. Corporate Governance (Bingley), 18 (2), 206–219. https://doi.org/10.1108/CG-10-2016- 0203

, , , & (2018). Board Meeting Frequency and Financial Performance: A Case of Listed Firms in Vietnam. International Journal of Business and Society, 19 (2), 464-472. https://core.ac.uk/download/pdf/188217226.pdf

, & (2020). Interdependence Relationship of Internationalization—Performance in Manufacturing Firms Listed in Indonesia Stock Exchange and Chinese Stock Exchanges. 115(Insyma), 416– 421. https://doi.org/10.2991/aebmr.k.200127.085

(1993). The Modern Industrial Revolution, Exit, and the Failure of Internal Control Systems. The Journal of Finance, 48 (3), 831–880. https://doi.org/10.1111/j.1540-6261.1993.tb04022.x

, & (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3, 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

, , & (2019). Ownership structure, board of directors and firm performance: evidence from Taiwan. Corporate Governance (Bingley), 19(1), 189–216. https://doi.org/10.1108/CG-04-2018- 0144

Komite Nasional Kebijakan Governance (KNKG). (2006). Pedoman Umum Good Corporate Governance. Jakarta.

, & (1992). A Modest Proposal for Improved Corporate Governance. The Business Lawyer, 48, 59–77.

, & (2001). The internationalization and performance of SMEs. Strategic Management Journal, 22 (6–7), 565–586. https://doi.org/10.1002/smj.184

, , & (2024). Good Corporate Governance In Non-Financial Sector Companies On The Indonesian Stock Exchange. JIAFE (Jurnal Ilmiah Akuntansi Fakultas Ekonomi), 10 (1), 13-22. https://doi.org/10.34204/jiafe.v10i1.9007

, & (2016). Does corporate governance beget firm performance in Fortune Global 500 companies? Corporate Governance (Bingley), 16(4), 747–764. https://doi.org/10.1108/CG-12-2015-0156

, & (2018). Board characteristics and firm value for Indian companies. Journal of Indian Business Research, 10 (1), 2–32. https://doi.org/10.1108/JIBR-07-2016-0074

(2021). The Effects of Corporate Governance on Company Performance and Dividends in Three Asean Countries. Media Ekonomi Dan Manajemen, 36(2), 230. https://doi.org/10.24856/mem.v36i2.2224

, , & (2021). Board Diversity and Financial Performance in Indonesia. Journal of Entrepreneurship & Business, 2 (2), 86–95. https://doi.org/10.24123/jeb.v2i2.4537

, , & (2021). The role of national culture in the impact of board gender diversity on firm performance: evidence from a multi-country study. Equality, Diversity and Inclusion, 40 (5), 631–650. https://doi.org/10.1108/EDI-04-2020-0092

, & (2020). Corporate governance performance and financial statement fraud: evidence from Malaysia. Journal of Financial Crime, 28 (3), 797–809. https://doi.org/10.1108/JFC-09-2020-0182

, , & (2017). Governance structures, voluntary disclosures and public accountability: The case of UK higher education institutions. Accounting, Auditing and Accountability Journal, 30 (1), 65–118. https://doi.org/10.1108/AAAJ-10-2014-1842

, , & (2018). Pengaruh Independensi, Kompetensi, dan Partisipasi Dewan Komisaris terhadap Kinerja Keuangan Perusahaan. Studi Akuntansi Dan Keuangan Indonesia, 1 (2), 210–231.

(2019). Internationalization effects on financial performance: The case of portuguese industrial SMEs. Journal of Small Business Strategy, 29 (3), 97–116.

, , , & (2015). Does gender matter? female representation on corporate boards and firm financial performance - A meta-analysis. PLoS ONE, 10 (6), 1–20. https://doi.org/10.1371/journal.pone.0130005

, & (2020). Corporate governance mechanisms and firm performance in a developing country. International Journal of Law and Management, 62 (2), 147–169. https://doi.org/10.1108/IJLMA-03-2019-0076

, , , & (2021). Corporate governance, ownership structure and firms’ financial performance: insights from Muscat securities market (MSM30). Journal of Financial Reporting and Accounting, 19 (4), 640–665. https://doi.org/10.1108/JFRA-05-2020- 0130

, & (2021). Board gender diversity, governance and Egyptian listed firms’ performance. Journal of Accounting in Emerging Economies, 12 (2), 279–299. https://doi.org/10.1108/JAEE-02-2021-0057

, , & (2020). The Effect of Gender Diversity on Company Financial Performance. Advances in Economics, Business and Management Research, 115, 470–475. https://doi.org/10.2991/aebmr.k.200127.094

(2019). Managerial ownership, board independence and firm performance. Accounting Research Journal, 32 (2), 203–220. https://doi.org/10.1108/ARJ-09-2017-0149

, & (2013). Internationalization and performance: A contextual analysis of Indian firms. Journal of Business Research, 66 (12), 2500–2506. https://doi.org/10.1016/j.jbusres.2013.05.041

, , & (2006). Do women in top management affect firm performance? A panel study of 2,500 Danish firms. International Journal of Productivity and Performance Management, 55 (7), 569–593. https://doi.org/10.1108/17410400610702160

(2020). A cross-firm analysis of corporate governance compliance and performance in Indonesia. Managerial Auditing Journal, 35 (5), 621– 643. https://doi.org/10.1108/MAJ-06-2019-2328

, , , & (2017). The impact of board independency, CEO duality and CEO fixed compensation on M&A performance. Corporate Governance (Bingley), 17 (5), 947–971. https://doi.org/10.1108/CG-03-2017-0047

, , & (2017). Corporate governance and ownership structure: Indonesia evidence. Corporate Governance (Bingley), 17 (2), 165–191. https://doi.org/10.1108/CG-12-2015-0171

, & (2015). Intensity on Firm Performance. Journal of Multinational Financial Management, 34, 1–18. http://dx.doi.org/10.1016/j.mulfin.2015.12.001