Rentabilidad de los Bancos Comerciales en Portugal y España: Un modelo de Análisis de Datos de Panel

Profitability of Commercial Banks in Portugal and Spain: A Panel Data Analysis Model

Marco Amaral

Instituto Politécnico do Cávado e do Ave (Portugal)

https://orcid.org/0000-0001-5014-3323

RESUMEN

El sistema bancario portugués y español, en el marco de la crisis económica y financiera sufrió una reducción significativa de la rentabilidad de su negocio bancario. Teniendo en cuenta el problema de la rentabilidad en el sector bancario a nivel mundial, algunos estudios han sido cada vez más destacados tanto en el mundo académico como en el mercado financiero. Así, este trabajo tiene como objetivo analizar los determinantes de la rentabilidad bancaria de los bancos que operan en dos sistemas financieros diferentes, Portugal y España, para los períodos de 2014 a 2019. Para obtener los resultados, se utilizó un modelo de análisis de datos de panel que combina datos de sección transversal (bancos) y de serie temporal (años), obteniendo un panel fuertemente equilibrado. A continuación, se utilizaron modelos de regresión lineal múltiple y fue posible identificar el riesgo de crédito, la solvencia y la eficiencia operativa como los principales factores explicativos de la rentabilidad bancaria. Finalmente, los resultados muestran que los altos indicadores de riesgo de crédito y eficiencia operativa de estos bancos tienen una influencia negativa significativa en su rentabilidad. A su vez, los indicadores de solvencia más robustos tienen un dominante significativo positivo en la rentabilidad de los bancos.

PALABRAS CLAVE

Desempeño; bancos; rentabilidad; sistema financiero; datos de panel.

ABSTRACT

The Portuguese and Spanish banking system, in the framework of the economic and financial crisis suffered a significant reduction in the profitability of its banking business. Taking into consideration the problem of profitability in the banking sector at a global level, some studies have been increasingly highlighted both in academia and in the financial market. Thus, this paper aims to analyze the determinants of banking profitability of banks operating in two different financial systems, Portugal and Spain, for the periods from 2014 to 2019. To obtain the results, we used a panel data analysis model that combines cross-section (banks) and time-series (years) data, obtaining a strongly balanced panel. Multiple linear regression models were then used and it was possible to identify credit risk, solvency and operational efficiency as the main factors explaining bank profitability. Finally, the results show that the high credit risk and operational efficiency indicators of these banks have a negative significant influence on their profitability. In turn, more robust solvency indicators have a positive significant dominant on bank´s performance.

KEYWORDS

Performance; banks; profitability; financial system; panel data.

Clasificación JEL: G21, N20.

MSC2010: 62H12, 62H15, 62H20, 91G70.

1. INTRODUCTION

In 2007, when the subprime crisis and the global financial crisis broke out, Portuguese and Spanish banks had excellent financial performance levels for their profitability indicators, providing a return on equity, measured by RoE (Return on Equity), of around 20.0 %, as well as a return on assets, measured by RoA (Return on Assets), of over 1 %. However, the effect of the global financial crisis, later aggravated from 2010 by the emergence of the sovereign debt crisis - “euro crisis”, which led to a series of financial assistance programmes (the Programme) to euro area countries (2010, Greece and Ireland; 2011, Portugal; 2012 Spain; and 2013 Cyprus), showed that the banking systems considered in this study (Portugal and Spain) were highly vulnerable to adverse economic contexts.

Among the various difficulties pointed out to the Portuguese and Spanish banking sector during this period, of particular note is the significant deterioration in the levels of profitability of the credit institutions of these two banking systems, which currently continue to be relatively low compared with the past (in 2019, RoE at levels below 8.0 % and RoA at levels below 1.0 %). For the authors Maudos (2012) and Costa (2016), this result essentially derives from four major problems conditioning the profitability of the banks under analysis, namely related with:

i) a large volume of non-performing assets, i.e., assets that do not generate income, especially non-performing loans (NPL);

ii) a significant part of assets that generate income, with emphasis on the exacerbated portfolios of mortgage loans with very low interest rate spreads and with long-term maturities;

iii) sustainability of the financial margin in significant reduction in a context of low interest rates; and

iv) the structure of banks’ operating costs in relation to the new business volume, leading to a deterioration of efficiency ratios (cost-to-income).

The aim of this paper is to analyze the determinants explaining the profitability of the seven largest commercial banks in the Portuguese and Spanish banking system, for the period from 2014 to 2019. To achieve this objective, we used the non-consolidated balance sheet data of the banks in the sample, which were obtained from the annual reports. For the purpose of analyzing the profitability of Portuguese and Spanish commercial banks, two indicators of bank profitability and related to financial ratios of the banks’ activity were used. These ratios allow working with a significant number of variables such as costs, revenues, loans, deposits, assets, capital, among others and relate them to their respective performance indicators, measured by RoA and RoE. Specifically, we strive to answer a set of questions that allow us to validate the level of profitability of two banking systems and to identify the divergences that exist between bank profitability and the internal characteristics of banks, such as: size, loans, credit risk, liquidity, solvency, operating efficiency and revenue diversification.

In this sense, it is expected that this study will provide strong contributions to research in this thematic area, essentially by analyzing the profitability of banking institutions in two distinct financial systems, thus allowing a portrait of the reality of Portuguese and Spanish banking, as well as to contribute to the teachings of bank profitability focused on its internal determinants.

The final document of this work is structured as follows, in addition to the first introductory section, a second section is presented concerning the literature review, offering a brief review of the existing literature in this area, with emphasis on the evidence of similar studies. Subsequently, the third point concerning the sample and methodology is presented, in which the methodology adopted in the research is described, presenting in a first stage, the sample and the statistical data treatment, moving on to the specification of the econometric model adopted and ending with the results obtained and their discussion. Finally, the fourth point is presented, the conclusion of the study, which reflects on the main conclusions of this research, as well as the main limitations of the study.

2. THEORETICAL FRAMEWORK AND HYPOTHESES TO BE TESTED

This section presents the theoretical framework of this study in order to ensure and substantiate the purposes of the work carried out, as well as the development of hypotheses to be tested through the hypotheses formulated for this purpose.

2.1 Literature review

There are several works that relate measures of financial performance of banks, namely, as to the determinants of profitability of credit institutions. Analyzing the literature for the banking market on bank profitability, the works carried out by authors such as Bourke (1989), Athanasoglou et al. (2008), Dietrich and Wanzenried (2011), Trujillo-Ponce (2013), Carvalho and Ribeiro (2016), Bikker and Vervliet (2018), Mota et al. (2019) and Pires et al. (2021), use as main indicators to measure the results and benchmark their assessments, the Return on Assets (RoA) and Return on Equity (RoE). To ensure the purposes of the present study, a set of data in different environments from several authors was analyzed. Thus, it was possible to distinguish some studies to the extent that the results obtained are distinct, but despite presenting mixed associated relationships, they keep in common combinations of internal and external determinants to explain bank profitability.

An earlier study by Bourke (1989) was among the first to directly relate bank profitability, as measured by RoA, with specific determinants of banking activity, either at the individual bank level through internal factors such as liquidity, capital and leverage, or at the industry/sector level through internal factors such as bank ownership and concentration. From the results obtained, the authors concluded that concentration has a significantly positive effect in explaining bank profitability, in contrast, capital and liquidity show a negative relationship with profitability.

In Europe, Athanasoglou et al. (2008) analyzed in light of the recent economic recession the profitability of Greek commercial banks, as measured by RoA and RoE, for the period 1985 to 2001. These authors performed the most popular decomposition of the determinants of bank profitability by adopting three categories of factors that explain bank profitability. First, through bank-specific factors, using variables such as size, capital, credit risk, loans, revenue diversification, bank type and efficiency and concluded a significant positive effect for the capital variable and a significant negative effect for the credit risk variable, while the results for bank size were insignificant. In a second category of determinants of bank profitability, they adopted industry/sector specific factors such as ownership and bank concentration and concluded that there is no clear relationship between industry concentration and bank profitability. Finally, in the third category of determinants, they addressed the macroeconomic environment (external factors) focusing on the economic growth variable measured by GDP – Gross Domestic Product. The authors concluded that strong economic growth combined with higher interest rates is likely to increase bank profitability.

Dietrich and Wanzenried (2011), in a study in the European zone, namely for Swiss banks, adopted three measures of bank profitability (RoA, RoE and NIM - Net Interest Margin), using a set of explanatory variables of internal factors (operating efficiency, funding costs, leverage, deposits, loans and revenue diversification) and external factors (GDP and a dummy variable for the financial crisis). From the results obtained, the authors concluded that the independent variables efficiency, funding costs, leverage and financial crisis have a negative effect on bank profitability, while the independent variables loans, deposits, revenue diversification and GDP have a positive effect on bank profitability.

In the same line of research, but now for a study in Spain, the author Trujillo-Ponce (2013), analyzed banks’ profitability (RoA and RoE) through a set of internal factors (capital, loans, size, revenue diversification) and external factors (GDP and inflation). The study concluded that in the case of the Spanish banking sector, revenue diversification shows a negative relationship with bank profitability, while the remaining variables show a significant positive relationship, with the exception of the size variable which is insignificant.

On the other side of the continent, namely in the US banking system, the study of the authors Bikker and Vervliet (2018), for the years 2001 to 2015, allowed considering an analysis of the period before and after the financial crisis. The work developed by the authors aims to explore the relationship between bank profitability and the economic environment of low interest rates. The sample includes a panel data set for 3,582 commercial and savings banks, and measures of profitability such as RoA, RoE, NIM and Profit were used. As determinants, the authors selected a set of bank-specific variables (size, loans, capital, credit risk and revenue diversification) and macroeconomic variables (GDP, inflation and interest rates). From the results obtained, the authors concluded that variables such as loans capital and size have the significant positive effect on bank profitability, in contrast, the credit risk variable has a negative effect and the macroeconomic variables GDP and inflation were found to be insignificant in explaining bank profitability. Finally, the authors confirm that partially, the environment of low interest rates hurt banks’ profitability and crush the net interest margin.

In Portugal, two recent studies by authors Carvalho and Ribeiro (2016) and Mota et al. (2019), were analyzed in periods occurring at different times in the Portuguese banking sector, i.e., between 2002 and 2012 and between 2006 and 2016, respectively. The authors based on bank profitability metrics (RoA, RoE and NIM), were able to obtain mixed results on the determinants explaining bank profitability. Thus, variables such as credit risk and leverage showed a significant negative effect on bank profitability for both studies. In turn, the banking concentration variable presents an opposite effect between the studies, while for the authors Carvalho and Ribeiro (2016) the concentration variable have a significant positive effect, for the authors Mota et al. (2019) the same variable presents a negative and insignificant effect. It should also be noted that the macroeconomic variable GDP, despite presenting in both studies a negative effect on bank profitability, in the study of Mota et al. (2019), unlike the Carvalho and Ribeiro (2016) study, is considered statistically significant to explain bank profitability, particularly in the period of the financial crisis when there was a weakening of the banking sector.

In an even more recent study, the authors Pires et al. (2021) analyzed the profitability of Portuguese banks for the period 2015-2018. To do this, they used the return on equity indicator measured by RoE as a measure of bank profitability for a sample of 18 banks operating in Portugal. The factors influencing bank profitability were separated into two groups, namely management quality, credit quality, capital adequacy and liquidity (internal bank factors), as well as GDP growth (external factor). Panel data was used to estimate the results for the grouped data using the linear regression model of the ordinary least squares method. The results obtained by the authors concluded that variables such as capital adequacy and credit quality have a significant negative effect and as such have a negative impact on bank profitability. On the other hand, the liquidity variable shows a positive and significant relationship with bank profitability, leading to the conclusion that liquidity has a positive influence on bank profitability.

Thus, considering that profitability is one of the most pertinent and current issues facing the Portuguese and Spanish banking sector and that there are only a few studies in this area, which leave previous researches with open questions in view of some mixed results obtained, it is understood that this study may have a strong contribution to the analysis and assessment of the determinants of profitability of credit institutions operating in Portugal and Spain. Thus, taking into consideration the studies analyzed, 7 hypotheses were developed to study the effect of each of them on bank profitability at credit institutions operating in Portugal and Spain. To this end, the seven largest Portuguese and Spanish banks were analyzed in the period from 2014 to 2019. For this work, two profitability measures (RoA and RoE) were adopted in order to analyze bank profitability, thus following the authors’ studies (Athanasoglou et al. 2006, 2008; Dietrich and Wanzenried, 2011; Trujillo-Ponce, 2013; Bikker and Vervliet, 2018, Rossi et al. 2018 and Mota et al. 2019). The determinants that may influence the profitability of banks, and that therefore relate with profitability, in light of the literature, the following hypotheses were developed.

2.2 Hypotheses to be tested

The seven hypotheses presented in this study concern the analysis of indicators and ratios directly related to the activity of the banking sector (internal factors), in order to show how the determinants can influence banking profitability. Table 1 below shows the development of the hypotheses to be tested in this research, by arguments (variables), as well as the authors who adopted them according to the literature review carried out.

Table 1 - Summary of research hypotheses

|

Argument (Variables) |

Authors (Year) |

Research Hypotheses |

|

Size (Total Net Assets) |

Demirgurç-Kunt and Huizinga (1999); Goddard et al. (2004); Athanasoglou et al. (2006;2008); Lagoa and Pina (2013); Shehzad et al. (2013); Barata (2014); Bikker and Vervliet (2018); Mogro and Bravo (2018); Rossi et al. (2018) and Pires et al. (2021). |

H1. There is a positive relationship between bank size and bank profitability. |

|

Loans (Loan Participation) |

Hermando and Nieto (2007); Athanasoglou et al. (2008); Garcia-Herrero et al. (2009); Dietrich and Wanzenried (2011); Trujillo-Ponce (2013); Barata (2014); Bikker and Vervliet (2018) and Rossi et al. (2018). |

H2. There is a positive relationship between loan share and bank profitability. |

|

Credit Risk (Credit Portfolio Quality) |

Demirgurç-Kunt and Huizinga (1999); DeYoung and Rice (2004); Athanasoglou et al. (2006;2008); Kosmidou (2008); Liang et al. (2013); Barata (2014); Carvalho and Ribeiro (2016); Sun et al. (2017); Bikker and Vervliet (2018); Rossi et al. (2018); Mota et al. (2019) and Pires et al. (2021). |

H3. There is a negative relationship between the quality of the loan portfolio and its profitability. |

|

Liquidity (Transformation Ratio) |

Bourke (1989); Molyneux and Thornton (1992); Demirgurç-Kunt and Huizinga (1999); Athanasoglou et al. (2006); Barth et al. (2013); Trujillo-Ponce (2013); Hamdi and Hakimi (2019) and Pires et al. (2021). |

H4. There is a positive (negative) relationship between bank liquidity and profitability. |

|

Solvency (Measured in terms of Accounting) |

Bourke (1989); Demirgurç-Kunt and Huizinga (1999); Athanasoglou et al. (2006;2008); Kosmidou (2008); Hoffmann (2011); Trujillo-Ponce (2013); Carvalho and Ribeiro (2016); Bikker and Vervliet (2018); Rossi et al. (2018) and Pires et al. (2021). |

H5. There is a positive (negative) relationship between a bank’s soundness and its profitability. |

|

Operating Efficiency (Cost-to-Income) |

Athanasoglou et al. (2006); Kosmidou (2008); Dietrich and Wanzenried (2011); Trujillo-Ponce (2013); Barata (2014); Basílio et al. (2016); Bitar et al. (2018) Rekiki and Kalai (2018); Rossi et al. (2018); Mota et al. (2019) and Pires et al. (2021). |

H6. There is a negative relationship between a bank’s operating efficiency and its profitability. |

|

Revenue Diversification (Commission) |

Elsas et al. (2010); Trujillo-Ponce (2013); Bikker and Vervliet (2018); Rossi et al. (2018) and Mota et al. (2019). |

H7. There is a positive (negative) relationship between the diversification of a bank’s revenue (commissions) and its profitability. |

Source: Own elaboration.

3. METHODOLOGY ADOPTED

This section presents the data analysis and description and the sample considered, followed by the variables included in the model and the treatment of the main statistical data, and ends with the specification of the econometric model.

3.1. Description of data and sample

For data collection in this study, we used content analysis of the statistical publications of APB - Associação Portuguesa de Bancos, AEB - Asociación Española de Banca and CECA - Cajas de Ahorros and also, of the mandatory publications of BdP - Banco de Portugal and BdE - Banco de España.

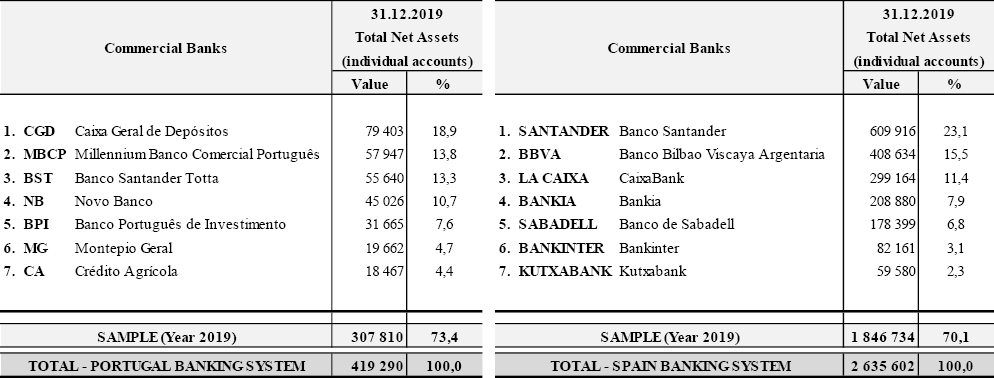

The sample considered is composed of the 7 largest banks in terms of volume of net assets (year 2019) operating in the Portuguese and Spanish banking system. Thus, 14 commercial banks were analysed, of which 7 are Portuguese and 7 are Spanish (4 from AEB and 3 from AECA), having been analyzed in this study the banks that made available the individual annual accounts during the period under analysis, i.e., 2014 to 2019. The total number of observations in the sample amounted to 168, for the two profitability indices under study (RoA and RoE), corresponding to 84 observations for each banking system in the sample.

In order to demonstrate the size of the two banking systems under study, a characterization of both systems is made (Table 2) consisting of the banks operating in Portugal and Spain, whose volume of net assets as at 31 December 2019 amounts to:

•EUR 419.3 billion, with the sample representing 73.4 % (EUR 307.8 billion) of all aggregate net assets in the Portuguese banking system; and

•€2.6 trillion, with the sample representing 70.1 % (€1.8 trillion) of all aggregate net assets in the Spanish banking system.

Table 2 - Characterization of the sample in the banking system in Portugal and Spain - 2019

Amounts in millions of euros, except when expressly indicated. Source: Own elaboration.

According to Table 2, the three largest commercial banks operating in the Portuguese and Spanish banking system represent 46 % and 50 %, respectively, of the total volume of net assets, as at 31 December 2019, revealing a high concentration of each of the banking systems.

3.2. Variables of the study

The dependent variables of bank profitability is in the present study measured by two alternative indicators, namely: Return on Assets (RoA) and Return on Equity (RoE).

From the literature reviewed in this work, it was understood that these are the indicators most widely adopted by the authors who address this issue. In addition, they are also indicators widely used by regulators and banks to assess a bank’s profitability.

Therefore, in order to better understand the evolution and behaviour of the RoA and RoE indicators for the two banking systems under analysis, historical data for some years not analysed in the study sample (2007, 2011, 2012 and 2013) and for the sample period considered in this study (2014 to 2019) are presented in Table 3 and 4:

Table 3 - Developments in dependent variables in the Portuguese banking system

|

RoA and RoE Historical Financial Data |

||||||||||

|

Not Considered in the Sample |

Period Considered in the Sample |

|||||||||

|

2007 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

|

|

RoA |

1.1 % |

–0.4 % |

–0.3 % |

–0.8 % |

–1.3 % |

0.2 % |

–0.6 % |

0.3 % |

0.7 % |

0.7 % |

|

RoE |

17.7 % |

–6.6 % |

–5.6 % |

–11.8 % |

–19.4 % |

2.1 % |

–8.0 % |

3.3 % |

7.1 % |

8.1 % |

Source: APB – Associação Portuguesa de Bancos: Summary of Banking Sector Indicators, April 2017 and April 2020.

Table 4 - Developments in dependent variables in the Spanish banking system

|

RoA and RoE Historical Financial Data |

||||||||||

|

Not Considered in the Sample |

Period Considered in the Sample |

|||||||||

|

2007 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

|

|

RoA |

1.1 % |

0.4 % |

–0.1 % |

0.3 % |

0.5 % |

0.5 % |

0.4 % |

0.6 % |

0.7 % |

0.5 % |

|

RoE |

21.2 % |

5.6 % |

–1.8 % |

4.4 % |

5.7 % |

5.6 % |

4.1 % |

6.1 % |

7.4 % |

7.0 % |

Source: AEB – Asociación Española de Banca: Results as at December 2015 and 2019.

The Portuguese and Spanish banking sector shows a trend towards improved banking profitability, being slightly higher in the case of the Portuguese banking system in the profitability indicator, measured by RoE (in 2019, 8.1 %, compared to 7.0 % in the Spanish banking sector). It should be noted, that the dispersion of these indicators among the banking systems under analysis, was more expressive in the Portuguese banking sector (illustrated in Table 3), with the loss of profitability showing negative values between 2011 and 2014, occurring a strong fall in the year 2014 (RoE, -19.4 %; RoA, -1.3 %), whose losses amounted to more than 5.4 billion euros. In turn, the Spanish banking sector (Table 4), after the outbreak of the financial crisis (2007) also recorded a loss in profitability, showing only losses in 2012 (RoE, -1.8 % and RoA, -0.1 %). In part, the losses resulted from the losses recognized in May of that year in the complex operation to reorganize the BANKIA financial group. In subsequent years, the stability of profitability indicators is observed accompanied even with a slight recovery (RoE, in 2013 of 4.4 %, increases in 2018 to 7.4 %). Finally, it should be noted for the high profitability of the banking sector indicators for the year 2007 (before the financial crisis), presenting values for RoE in Portugal of 17.7 % and for Spain of 21.2 %, while RoA in both banking systems with values of 1.1 %. After these 12 years, Portuguese and Spanish banks are still a long way from achieving the banking profitability of other good old days.

Taking into consideration the results obtained in the studies listed in the theoretical framework of this paper and which are concerned with identifying the determinants of bank profitability, independent variables were selected that are thought to influence the dependent variable, and therefore relate to bank profitability. The independent variables used in this study are reflected in the previously formulated hypotheses and are indicators and ratios related to banking sector activity and represent a set of variables that identify seven determining factors. The variables included in the model, as well as their form of determination and the expected signs for the regression coefficients of the explanatory variables of the hypotheses to be tested are as follows (Table 5).

Table 5 - Variables included in the model

|

Variables |

Notation |

Form of Determination |

Hypothesis and Expected Sign |

|

Dependent: Return on Assets |

RoA |

RoA Ratio (Return on Assets) = Net Profit / Net Assets |

|

|

Return on Equity |

RoE |

RoE Ratio (Return on Equity) Net Profit / Equity Capital |

|

|

Independent: Size |

LOGSZ |

Logarithm (natural) = of Net Asset Value |

H1 (+) |

|

Loans |

LOAN |

Loan Share = Net Loans to Customers / Net Assets |

H2 (+) |

|

Credit Risk |

CRER |

Degree of Impairment of Loans and advances to Customers = Loans Impairment (year) / Net Loans to Customers |

H3 (-) |

|

Liquidity |

LIQ |

Transformation Ratio = Net Loans to Customers / Customers Deposits |

H4 (+/-) |

|

Solvency |

SOLV |

Solvency Ratio (in accounting terms) = Equity Capital / Net Assets |

H5 (+/-) |

|

Operating Efficiency |

EFIOP |

Cost-to-Income Ratio = Structural Costs / Banking Product |

H6 (-) |

|

Revenue Diversification |

DIVER |

Commission = Net Commissions / Banking Product |

H7 (+/-) |

Source: Own elaboration.

3.3 Descriptive statistics

The data in the present paper includes the descriptive statistics analyses of the dependent variables (bank profitability indices) and the independent variables (determinants of bank profitability) in the set of six years analyzed in the present study (2014-2019).

•Bank profitability indices

The data of the descriptive statistics of banking profitability measured by return on assets (RoA) and return on equity (RoE), can be seen in Table 6.

Table 6 - Descriptive statistics for RoA and RoE in Portugal and Spain

|

RoA – Return on Assets |

|||||||||||||

|

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

||

|

Portugal |

Spain |

||||||||||||

|

0.0 |

0,5 |

||||||||||||

|

Average |

–0.3 |

–0.1 |

–0.3 |

0.0 |

0.1 |

0.2 |

0.4 |

0.4 |

0.4 |

0.5 |

0.5 |

0.6 |

|

|

Median |

–0.3 |

0.3 |

0.0 |

0.1 |

0.6 |

0.7 |

0.3 |

0.5 |

0.4 |

0.5 |

0.5 |

0.6 |

|

|

S. D. |

0.4 |

1.0 |

1.1 |

1.3 |

1.5 |

1.2 |

0.2 |

0.2 |

0.2 |

0.2 |

0.1 |

0.1 |

|

|

Min. |

–0.8 |

–1.7 |

–2.0 |

–2.7 |

–3.2 |

–2.3 |

0.1 |

0.2 |

0.2 |

0.2 |

0.3 |

0.3 |

|

|

Max. |

0.3 |

1.0 |

0.8 |

1.3 |

1.6 |

1.0 |

0.7 |

0.7 |

0.8 |

0.7 |

0.7 |

0.7 |

|

|

Nr. Obs. |

7 |

7 |

7 |

7 |

7 |

7 |

7 |

7 |

7 |

7 |

7 |

7 |

|

|

∑RoA |

42 observations |

42 observations |

|||||||||||

|

RoE – Return on Equity |

|||||||||||||

|

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

||

|

Portugal |

Spain |

||||||||||||

|

–0.8 |

6.0 |

||||||||||||

|

Average |

–4.3 |

–0.1 |

–5.9 |

0.8 |

1.6 |

2.8 |

5.2 |

5.5 |

5.9 |

6.0 |

6.6 |

7.3 |

|

|

Median |

–5.4 |

4.1 |

0.5 |

0.6 |

6.0 |

7.7 |

3.9 |

3.9 |

4.6 |

5.5 |

6.0 |

6.0 |

|

|

S. D. |

6.9 |

13.5 |

20.8 |

14.9 |

17.6 |

13.6 |

3.6 |

3.1 |

3.8 |

2.7 |

2.4 |

2.7 |

|

|

Min. |

–13.2 |

–18.1 |

–47.9 |

–28.9 |

–36.5 |

–26.5 |

1.1 |

2.7 |

3.0 |

3.7 |

4.8 |

4.4 |

|

|

Max. |

7.0 |

19.7 |

11.9 |

19.8 |

15.3 |

14.3 |

11.8 |

10.4 |

14.3 |

11.6 |

11.9 |

11.4 |

|

|

Nr. Obs. |

7 |

7 |

7 |

7 |

7 |

7 |

7 |

7 |

7 |

7 |

7 |

7 |

|

|

∑RoE |

42 observations |

42 observations |

|||||||||||

|

∑ |

84 observations |

84 observations |

|||||||||||

|

Total |

168 observations |

||||||||||||

Values in percentage, except when expressly indicated. Source: Own elaboration based on STATA 13.1 results.

It can be seen that bank profitability, measured by RoA and RoE, for the period under review, in the two banking systems is slightly improving, i.e., rising. In the case of Portugal’s commercial banks, it is observed that between 2014 to 2019 the average of the profitability indices move from negative (losses) to positive. Thus, the RoA, from -0.3 % in 2014, passes to 0.2 % in 2019, which makes an average profitability of nil for 6 years of the period under analysis, while the RoE, from -4.3 % in 2014, passes to 2.8 % in 2019, making an average negative profitability of -0.8. Like the Portuguese banking market, banking profitability in Spain increased in the sample period, however in a more accentuated and stable manner, as there are no negative indicators. Thus, the average value of RoA grew from 0.4 % in 2014 to 0.6 % in 2019, while, RoE had an average growth from 5.2 % in 2014 to 7.3 % in 2019. In average terms, the profitability indices in Spain in the period under review show a RoA of 0.5 % and a RoE of 6.0 %.

•Determinants of banking profitability

With regard to the statistical data of the seven internal factors analyzed in this study and which are directly related to the activity of the Portuguese and Spanish banking sector, the following can be observed, as shown in Table 7:

Table 7 - Descriptive statistics for internal factors in Portugal and Spain

|

Determinants of Bank Profitability |

|||||||||||||

|

Obs |

Average |

P50 |

S.D. |

Min. |

Max. |

Obs |

Average |

P50 |

S.D. |

Min. |

Max. |

||

|

Portugal |

Spain |

||||||||||||

|

logsz |

42 |

7.6 |

7.7 |

0.3 |

7.2 |

8.0 |

42 |

8.2 |

8.3 |

0.7 |

4.4 |

8.8 |

|

|

loan |

42 |

62.4 |

63.5 |

8.8 |

47.6 |

86.6 |

42 |

60.5 |

64.9 |

12.7 |

35.5 |

76.6 |

|

|

crer |

42 |

1.2 |

0.9 |

1.5 |

–2.4 |

5.5 |

42 |

0.4 |

0.4 |

0.4 |

0.0 |

1.5 |

|

|

liq |

42 |

93.9 |

91.6 |

16.2 |

64.6 |

125.0 |

42 |

103.9 |

102.6 |

10.1 |

86.5 |

129.7 |

|

|

solv |

42 |

7.8 |

8.0 |

1.6 |

4.1 |

10.8 |

42 |

8.0 |

7.4 |

2.3 |

5.2 |

14.3 |

|

|

efiop |

42 |

62.0 |

57.4 |

20.6 |

33.4 |

119.8 |

42 |

52.7 |

53.3 |

7.5 |

38.2 |

71.4 |

|

|

diver |

42 |

30.4 |

29.2 |

11.8 |

13.1 |

73.4 |

42 |

24.9 |

24.1 |

5.7 |

15.8 |

38.2 |

|

Values in percentage, except when expressly indicated. Source: Own elaboration based on STATA 13.1 results.

The statistical description of the independent variables (Table 7) shows that, on average, Spanish banks show better solvency, that is, more robust capital adequacy ratios (8.0 % against 7.8 % for Portuguese banks), as well as better efficiency and rationalization of operating costs, on average (52.7 % against 62.0 %) and they are on average bigger size - logsz, (8.2 against 7.6). It can be seen that the credit risk variables - rcre and emp loan share - show, on average, higher values in Portuguese banks (1.2 % and 62.4 %, respectively, against 0.4 % and 60.5 % in Spanish banks). With regard to the independent variable of liquidity - liq, it can be inferred that in the period under analysis, Portuguese banks show a lower level of transformation of customer resources into credit granted than Spanish banks (93.9 % against 103.9 %). Finally, the revenue diversification variable - diver (complementary activity - commissions), registered higher average values in Portuguese banks (30.4 %, against 24.9 % in Spanish banks).

3.4 Specification of the econometric model

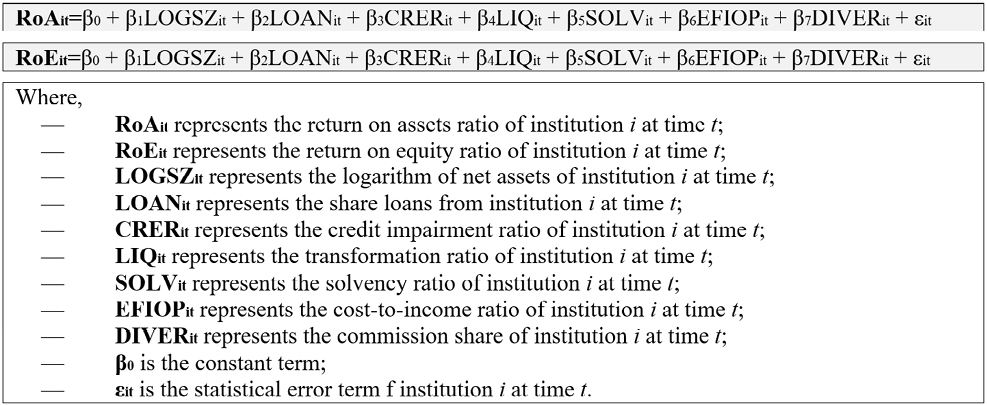

The works that evaluate the factors that determine the profitability of banking institutions, such as Trujillo-Ponce (2013), Carvalho and Ribeiro (2016), Bikker and Vervliet (2018), Rossi et al. (2018), Hamdi and Hakimi (2019), Mota et al. (2019), Pires et al. (2021) and Chadi and Rasha (2022), use, fundamentally, linear regression models, which allow to describe and evaluate which independent variables have explanatory power on the dependent variables. Thus, to answer the seven hypotheses previously mentioned, the following linear regression models were developed, as shown in Table 8:

Table 8 - Linear regression models

Source: Own elaboration.

3.5 Results and discussion

In the econometric estimation of the model, the Panel Data (Stata 13.1 - Statistics Data Analysis) technique was used, which combines cross-section (banks) and time-series (years) data, and a strongly balanced panel was obtained. In order to model the functional relationship between the variables, multiple linear regression models were used, through the panel data model, and the Hausman test was applied, in order to assess whether this method fits better the fixed effects model or the random effects model. For the estimation of the econometric results, first of all, the problems of multicollinearity among the independent variables of the model were assessed. Thus, the correlation matrix between the variables was determined in order to assess whether there are indirect effects between the variables of the study, and it was observed that there are no problems of this nature. Secondly, a regression was carried out using panel data treatment, through the fixed-effects Ordinary Least Square (OLS regression) model and also through the Random-effects Generalized Least Squares (GLS regression) model. From the analysis carried out, it was found that the model with the highest quality is that which is used through the fixed-effects model. According to Wooldridge (2002), the random effects model is more efficient in large samples, because the random effects estimators present lower standard errors; however, the fixed effects model is intended to be robust as to the correlation between the independent variables and the unobserved effects.

3.5.1 Estimation of econometric results

Before presenting the estimated results and in order to simplify the analysis of the selected variables, the correlation matrices of the different variables of the study are presented. Table 9 shows the correlation matrix of the independent variables for both Portuguese and Spanish banks.

Table 9 - Correlation matrix of the independent variables

|

Logsz |

Loan |

Crer |

liq |

solv |

efiop |

diver |

|

|

Portugal |

|||||||

|

logsz |

1 |

– |

– |

– |

– |

– |

– |

|

loan |

0.2668 |

1 |

– |

– |

– |

– |

– |

|

crer |

0.1109 |

–0.1338 |

1 |

– |

– |

– |

– |

|

liq |

0.2316 |

0.4824 |

0.1045 |

1 |

– |

– |

– |

|

solv |

–0.0864 |

–0.3373 |

–0.0840 |

–0.2419 |

1 |

– |

– |

|

efiop |

–0.2371 |

–0.2200 |

–0.1923 |

–0.1949 |

0.1384 |

1 |

– |

|

diver |

0.0936 |

0.0324 |

–0.1030 |

–0.0539 |

0.2934 |

0.7220 |

1 |

|

Spain |

|||||||

|

logsz |

1 |

– |

– |

– |

– |

– |

– |

|

loan |

–0.5159 |

1 |

– |

– |

– |

– |

– |

|

crer |

0.0400 |

–0.0500 |

1 |

– |

– |

– |

– |

|

liq |

–0.4862 |

0.5999 |

0.2625 |

1 |

– |

– |

– |

|

solv |

0.3277 |

–0.5906 |

–0.0795 |

–0.4960 |

1 |

– |

– |

|

efiop |

0.2464 |

0.0188 |

–0.4755 |

–0.5133 |

0.2877 |

1 |

– |

|

diver |

–0.1481 |

0.4550 |

–0.4786 |

–0.3036 |

–0.0933 |

0.6397 |

1 |

Source: Own elaboration.

By analyzing Table 9, we conclude that the correlation coefficients in general are not significantly high (less than 75 %) to cause concern about multicollinearity problems.

For the estimation of the model it is necessary to take into account in this study that the data treatments used are arranged in a longitudinal panel, composed of a set of several entities (N=7 banks) and over several periods of time (T=6 years), according to table 10:

Table 10 - Regressions - results of bank estimates in Portugal and Spain

|

Variable |

Portugal |

Spain |

||||||

|

RoA (Return on Assets) |

RoE (Return on Equity) |

RoA (Return on Assets) |

RoE (Return on Equity) |

|||||

|

Fixed Effects |

Fixed Effects |

|||||||

|

Coef. |

Sig |

Coef. |

Sig |

Coef. |

Sig |

Coef. |

Sig |

|

|

Logsz |

0.4997 |

0.743 |

2.752 |

0.919 |

–.0281 |

0.572 |

–.4249 |

0.504 |

|

Loan |

0.0015 |

0.893 |

–.1422 |

0.483 |

.0025 |

0.858 |

.0286 |

0.873 |

|

Crer |

–.2927 |

0.000 (c) |

–4.598 |

0.000 (c) |

–.2194 |

0.034 (b) |

–2.548 |

0.052 (a) |

|

Liq |

0.0086 |

0.141 |

.0783 |

0.449 |

–.0080 |

0.188 |

–.1262 |

0.108 |

|

Solv |

0.1681 |

0.005 (c) |

2.642 |

0.012 (b) |

.0325 |

0.361 |

–.1958 |

0.666 |

|

Efiop |

–.0221 |

0.001 (c) |

–.3092 |

0.008 (c) |

–.0071 |

0.277 |

–.1078 |

0.202 |

|

Diver |

0.0070 |

0.553 |

.0710 |

0.735 |

–.0042 |

0.769 |

–.0310 |

0.868 |

|

_cons |

–4.589 |

0.703 |

–18.66 |

0.931 |

1.688 |

0.141 |

30.11 |

0.043 |

|

Nr. Observations: |

42 |

42 |

42 |

42 |

||||

|

Nr. Banks: |

7 |

7 |

7 |

7 |

||||

|

R-sq: |

Within |

0.8336 |

0.7917 |

0.2731 |

0.2670 |

|||

|

Between |

0.2687 |

0.5812 |

0.0580 |

0.1161 |

||||

|

Overall |

0.4252 |

0.5676 |

0.1248 |

0.1628 |

||||

|

F(7,28) |

20.03 |

15.20 |

1.50 |

1.46 |

||||

|

Prob>F |

0.0000 |

0.0000 |

0.2069 |

0.2230 |

||||

|

Hausman Test: |

||||||||

|

chi² |

60.79 |

147.40 |

6.81 |

21.38 |

||||

|

Prob> chi² |

0.0000 |

0.0000 |

0.4488 |

0.0033 |

||||

|

Nota: |

(a) (b) (c) Statistically significant results for a significance level of 0.10, 0.05 and 0.01 respectively. |

|||||||

Source: Own elaboration.

The results obtained through the multivariate regressions indicate that there is an important level of explanation of the determinants for the two banking profitability indicators used in this study.

In the case of the Portuguese banking sector the RoA and RoE with an adjusted R² of 42.52 % and 56.76 %, respectively, and in the case of the Spanish banking sector an adjusted R² of 12.48 % and 16.28 % is observed for the profitability indicators of RoA and RoE, respectively. With regard to the explanatory variables of the two models used in this study, the results obtained show three variables with explanatory power of banking profitability. In this context, statistical significance is recognized in explaining banking profitability both measured by RoA and RoE of the variables of credit risk (CRER), solvency (SOLV) and operating efficiency (EFIOP).

3.5.2 Discussion of results

Thus, the results of the hypotheses to be tested are as follows:

H1. There is a positive relationship between bank size and bank profitability.

According to the literature review, most of the authors’ studies concluded that there is a positive relationship between bank profitability and bank size. For Berger et al. (2000) the increase in banking profitability may occur with bank size because some customers prefer services from larger institutions. The authors McKillop et al. (2002) point to the importance of economies of scale, since larger banks can produce with lower unit costs, which can be seen in the use of technology and information systems for cross-selling financial products and services. By examining the coefficients of the two dependent variables of the two banking systems, it can be seen that the explanatory variable of size (LOGSZ) measured by the natural logarithm of the value of total net assets is not a determining factor influencing bank profitability, i.e., this variable has no significant influence on the profitability of commercial banks. In the case of the Spanish banking sector, the variables RoA and RoE evidence a negative relationship and, therefore, not compatible with the results and opinions of most authors exposed in the theoretical framework. This situation is explained by the strong banking restructuring (Known as FROB – Bank Resolution Fund) that took place in the Spanish banking system and that translated into the intervention of a wide range of commercial and savings banks that were involved in growth processes involving mergers and acquisitions, and whose main objective was to strengthen solvency rather than increase the profitability of Spanish banks. Thus, hypothesis 1 cannot be validated.

H2. There is a positive relationship between loan share and bank profitability.

For Garcia-Herrero et al. (2009) a bank’s profitability should increase with a higher share of loans in assets, provided that interest rates on loans are applied at adjusted prices. In the same line of thought, authors Bikker and Vervliet, (2018), refer that a large loan portfolio increases banks’ profitability. The results obtained show that the loan share variable (LOAN) has no significant influence on bank profitability. In the case of the Portuguese banking system, bank profitability indicators show a mixed association. The main reason for this fact may be associated with the demands of capital requirements for certain credit operations. Therefore, this may be a field to deepen on the obtained results and considerably extend the research on this matter. Thus, we cannot validate hypothesis 2.

H3. There is a negative relationship between the quality of the loan portfolio and its profitability.

According to the literature reviewed, the authors concluded that this variable, considered to be specific to the sector of activity, is one of the variables that most influences bank profitability. Thus, a lower quality of the loan portfolio negatively affects bank profitability with the amount of provisioning for expected credit losses. The results lead to the conclusion that the explanatory variable of the model concerning credit risk (CRER) contributes to the decrease in profitability of banks in Portugal and Spain. The regression coefficients for the variables RoA and RoE show a negative and statistically significant sign, and in the case of the Portuguese banking sector for a significance level of both indicators of 1 % (Sig = 0.000). In the case of the Spanish banking sector for a significance level of 5 % (Sig = 0.034) for the RoA indicator and for a significance level of 10 % (Sig = 0.052) for the RoE indicator. These results are in agreement with the empirical evidence of the authors, Demirguç-Kunt and Huizinga, (1999), Athanasoglou et al., (2006; 2008), Kosmidou, (2008), Carvalho and Ribeiro, (2016), Bikker and Vervliet, (2018), Rossi et al., (2018) and Mota et al. (2019). Thus, it is possible to validate for both banking systems hypothesis 3.

H4. There is a positive (negative) relationship between liquidity and bank profitability.

This indicator is widely used by regulators to assess banks’ liquidity. The higher this indicator, the greater the possibility of a bank generating income, and therefore becoming more profitable, however, the less liquid the bank will be to honour the capital of depositors, institutions and other customers. Banking profitability varies with banks’ liquidity, the results obtained show that, the independent variable of liquidity (LIQ) has a positive and negative relationship on banks’ profitability. These results are in line with the authors’ studies evidenced in the literature review, but given that they do not show a statistically significant influence for both banking systems under analysis, hypothesis 4 is not valid.

H5. There is a positive (negative) relationship between a bank’s soundness and its profitability.

Given the difficulty in obtaining data from the sample banks, the indicator used was the financial data obtained from the Balance Sheet resulting from the ratio between equity and total net assets (solvency understood in accounting terms). The higher this ratio is, the better, demonstrating on the one hand, a greater capacity for banks to cover losses on their assets and, on the other hand, a lower need to raise external resources, and therefore greater profitability for the bank. In the case of the Portuguese banking sector, the sign of the regression coefficient of the two profitability indicators is positive and statistically significant for RoA, with a statistical significance level of 1 % (Sig = 0.005) and for RoE, with a statistical significance level of 5 % (Sig = 0.012), therefore an increase in the solvency indicator contributes to an increase in banks’ profitability. In turn, in the case of the Spanish banking sector, the results obtained from the independent variable (SOLV) is not a determining factor that can impact on banks’ profitability. However, the results allow to verify a mixed relationship (positive for the variable RoA and negative for the variable RoE) according to expected signs. This result is convergent with the studies of authors Bourke, (1989) Hoffmann, (2011), Carvalho and Ribeiro (2016) and Rossi et al., (2018) who concluded a negative relationship and with the studies of authors Demirguc-Kunt and Huizinga, (1999), Athanasoglou et al., (2006; 2008), Kosmidou, (2008), Trujillo-Ponce, (2013), Bikker and Vervliet, (2018) and Pires et al., (2021) who concluded a positive relationship. Thus, it is also possible to validate hypothesis 5.

H6. There is a negative relationship between a bank’s operating efficiency and its profitability.

This indicator measures each bank’s operating efficiency, i.e., how efficiently it manages its structural costs. The lower this indicator, the better the efficiency and rationalization of the banking companies’ structural expenses for each period, and consequently, the higher the results. The estimated results allow for the validation of hypothesis 6 for the two banking systems under study since it presents the expected sign (negative), however, it is only statistically significant for the Portuguese banking sector, with a statistical significance level of 1 % for the indicators of RoA (Sig = 0.001) and RoE (Sig = 0.008). It can therefore be concluded that the operating efficiency (EFIOP) of Portuguese commercial banks in terms of the ratio of operating expenses to gross income has a significant influence on bank profitability. This result is in agreement with the empirical evidence of the authors Kosmidou, (2008), Dietrich and Wanzenried (2011), Trujillo-Ponce, (2013), Barata (2014), Bitar et al., (2018), Rekik and Kalai, (2018), Rossi et al., (2018), Mota et al. (2019) and Pires et al., (2021) who concluded the existence of a negative association between the operating efficiency ratio and bank profitability.

H7. There is a positive (negative) relationship between a bank’s revenue (commission) diversification and its profitability.

Recently, reflecting the low interest rates prevailing in the market, banks have targeted non-interest income, or commission income as an important source of future revenue. The existing literature reveals two divergent empirical evidences on the relationship between revenue diversification (measured by the ratio of banks’ commissions to their banking product) and bank profitability. When analyzing the regression coefficients of the variables RoA and RoE it is observed that, the independent variable of revenue diversification (DIVER) measured by the ratio between net commissions and banking product is not a determining factor that can impact on the profitability of Portuguese and Spanish banks. Thus, hypothesis 7 cannot be validated.

4. CONCLUSION AND LIMITATION OF THE STUDY

Although in a more recent period there has been some recovery in banking profitability, the profitability indicators of banks still show low levels.

This paper aims to analyze the impact of some specific factors of the banking sector on the profitability of Portuguese and Spanish banks for the period 2014 to 2019. To this end, two econometric models were built, in which the determinants of bank profitability are explained, and can be used to predict them. Two dependent variables (return on assets and return on equity indicators) and seven independent variables (size, loans, credit risk, liquidity, solvency, operating efficiency and revenue diversification) were used to estimate the determinants of Portuguese and Spanish banks’ profitability.

Thus, several conclusions emerge from this study. Thus, for a total of 168 observations corresponding to 14 commercial banks, the explanatory variable of credit risk (CRER) is the one that presents the best results in explaining the banking profitability ratios (RoA and RoE) for the two banking systems analyzed. In the case of the Portuguese banking system, the variable (CRER) presents a statistical significance level of 1 % and in the case of the Spanish banking system, the same variable is statistically significant, for a significance level of 5 % (Sig = 0.034) and 10 % (Sig = 0.052) for RoA and RoE, respectively. The credit risk variable (CRER), presents for the two banking profitability indicators and for the two banking systems with a negative relationship. Thus, one may infer that a worse quality of the credit portfolio negatively influences the profitability of Portuguese and Spanish commercial banks.

The study confirms that the results of the solvency independent variable (SOLV), presents in the case of the Portuguese banking sector statistically significant for a significance level of 1 % (Sig = 0.005) in the bank profitability index, measured by RoA. The same occurs in the bank profitability index, measured by RoE; however, the statistical significance level is 5 % (Sig = 0.012). It is also found that the variable (SOLV) presents a positive association with the variables of bank profitability. Thus, it can be inferred that an increase in Portuguese banks’ solvency positively influences bank profitability.

The results show that the independent variable of operating efficiency (EFIOP) is only statistically significant at a 1 % significance level for the Portuguese banking sector. Banking profitability shows a negative relationship with this variable, inducing that the profitability of Portuguese banks is influenced by an increase in operating expenses.

By individual analysis of the p> |z| test, the explanatory variables of size (LOGSZ), as well as the liquidity variable (LIQ), the loan participation variable (LOAN) and the revenue diversification variable (DIVER) are not determinant factors influencing the profitability of commercial banks in the two banking systems analyzed.

It can be concluded that the profitability of Portuguese and Spanish banks can be explained by different factors related to banks’ specific activity (internal determinants). Lower credit risk transformation (CRER), together with higher operating efficiency (EFIOP), may translate into higher profitability for banks. The results also emphasize the benefits of robust equity strength (SOLV).

The results of this study can be useful for bank decision makers as well as banking supervisors and regulators as they identify valuable guidance on the effect of key financial variables on a bank’s profitability. It may also be used to develop a framework of policies and regulations affecting bank financial performance.

The study has, however, some limitations, as the sample used is very small, limited to the seven largest banks in the Portuguese and Spanish banking systems. In addition, the period of analysis is relatively short (6 years), so the results should be analyzed taking into account this limitation.

Thus, we suggest, for future research, extending the sample and the period of analysis and considering other indicators, both of financial nature (capital adequacy measured by Tier 1, technology systems or corporate governance) and of non-financial nature (GDP, interest rates or inflation), which may potentially explain bank profitability.

AKNOWLEDGEMENTS

The author is grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article.

FUNDING

This research has not received any specific grants from funding agencies in the public, commercial or non-profit sectors.

REFERENCES

Asociación Española de Banca, AEB (2015). Resultados a diciembre de 2015.

Asociación Española de Banca, AEB (2019). Resultados a diciembre de 2019.

Associação Portuguesa de Bancos, APB (2017). Indicadores do Setor Bancário Anual 2016.

Associação Portuguesa de Bancos, APB (2020). Indicadores do Setor Bancário Anual 2019.

; , (2008). Bank-specific, industry-specifc and macroeconomic determinants of bank profitability. Journal of International Financial Markets, Institutions & Money, 18(2), 121-136. http://dx.doi.org/10.1016/j.intfin.2006.07.001

; , (2006). Determinants of bank profitability in the South Eastern European region. Munich Personal RePEc Archive, 1-31.

, (2014). Determinantes da Rendibilidade Bancária – Um estudo empírico. Revista Inforbanca 102(outubro-dezembro), 26-28.

; ; ; ; (2013). Do bank regulation, supervision and monitoring enhance or impede bank efficiency? Journal of Banking and Finance, 37, 2879-2892. https://doi.org/10.1016/j.jbankfin.2013.04.030

; ; (2016). Portuguese banks performance: comparing efficiency with their Spanish counterparts. Eurasian Economic Review, 6, 27-44. https://doi.org/10.1007/s.40822-015-0033-6

, , , (2000). Globalization of financial institutions: evidence from cross-border banking performance. Brookings-Wharton Paper on Financial Services, p. 23-120.

; (2018). Bank profitability and risk-taking under low interest rates. International Journal of Finance & Economics, 23, 3-18. https://doi.org/10.1002/ijfe.1595

; ; (2018). The Effect of capital ratios on the risk, efficiency and profitability of banks: evidence from OECD countries. Journal of International Financial Markets, Institutions and Money, 53, 227-262. https://doi.org/10.1016/j.intfin.2017.12.002

(1989). Concentration and other determinants of bank profitability in Europe, North America and Australia. Journal of Banking and Finance, 13(1), 65-79. https://doi.org/10.1016/0378-4266(89)90020-4

; (2016). Fatores explicativos da rendibilidade do setor bancário: evidência empírica em Portugal. Estudos do ISCA, série IV, 13, 1-11. https://doi.org/10.34624/ei.v0i13.4729

; (2022). Internal financial determinants of stock prices in the banking sector: comparative evidence from Dubai and Abu Dhabi Stock markets. Revista de Métodos Cuantitativos para la Economía y la Empresa, 34, 3-16. https://orcid.org/0000-0003-2995-9533

, (2016). O ajustamento do sistema bancário português: evolução e desafios futuros. Intervenção do Governador do Banco de Portugal na Conferência da Associação Portuguesa de Bancos. “O presente e o futuro do setor bancário”, realizada el 17 mayo.

; (1999). Determinants of commercial bank interest margins and profitability: some international evidence. World Bank Economic Review, 13(2), 379-408. https://doi.org/10.1093/wber/13.2.379

; (2004). Non interest income and financial performance at US comercial banks. The Financial Review, 39, p. 101-127. https://doi.org/10.1111/j.0732-8516.2004.00069.x

; (2011). Determinants of bank profitability before and during the crisis: evidence from Switzerland. Journal of International Financial Markets, Institutions and Money, 21(3), 307-327. https://doi.org/10.1016/j.intfin.2010.11.002

; ; (2010). The anatomy of bank diversification. Journal of Banking and Finance, 34(6), 1274-1287 https://doi.org/10.1016/j.jbankfin.2009.11.024

; ; (2009). What explains the low profitability of Chinese banks?. Journal of Banking and Finance, 33, 2080-2092. https://doi.org/10.1016/j.jbankfin.2009.05.005

; , (2004). Dynamics of growth and profitability in banking. Journal of Money, Credit and Banking, 36(6), 1069-1090. https://doi.org/10.1353/mcb.2005.0015

; (2019). Does liquidity matter on bank profitability? Evidence from a nonlinear framework for a large sample. Business and Economics Research Journal, 10(1), 13-26. https://doi.org/10.20409/berj.2019.153

; (2007). Is the internet delivery channel changing banks performance? The case of Spanish banks. Journal of Banking and Finance, 31, 1083-1099. https://doi.org/10.1016/j.jbankfin.2006.10.011

(2011). Determinants of the profitability of the US banking industry. International Journal of Business and Social Science, 2(22), 255-269.

(2008). The determinants of banks profits in Greece during the period of EU financial integration. Managerial Finance, 34(3), 146-159. https://doi.org/10.1108/03074350810848036

; (2013). Size and profitability in cooperative banking. DINÂMIA´CET – IUL and Dept. of Political Economy, ISCTE – University Institute of Lisbon, WP/08, 1-25.

; , (2013). Enhancing bank performance through branches or representative offices? Evidence from European banks. International Business Review, 22(3), 495-508.

(2012). El impacto de la crisis en el setor bancario español. Cuadernos de Información Económica, 226, Fundación de Las Cajas de Ahorros (FUNCAS), 155-164.

; , (2002). Investigating the cost performance of UK credit unions using radial and non-radial efficiency measures. Journal of Banking and Finance, 26, 1563-1591.

; (2018). Assessing competition in the private banking sector in Ecuador: an econometric approach with the Panzar-Rosse model. Cuadernos de Economía, 41, 225-240.

; (1992). Determinants of European bank profitability: a note. Journal of Banking and Finance, 16(6), p. 1173-1178. https://doi.org/10.1016/0378-4266(92)90065-8

; ; (2019). Determinantes da rentabilidade bancária: evidências para os maiores bancos portugueses. European Journal of Applied Business Management, 5(2), 78-96.

; ; (2021). Determinants of Portuguese banks profitability: an update. Tourism & Management Studies, 17(3), 63-70. https://doi.org/10.18089/tms.2021.170305

; (2018). Determinants of banks profitability and efficiency: empirical evidence from a sample of banking systems. Journal of Banking and Financial Economics, 1(9), 5-23. https://doi.org/10.7172/2353-6845.jbfe.2018.1.1

; ; ; (2018). Determinants of bank profitability in the Euro Area: what has changed during the recent financial crisis? International Business Research, 5(11), 18-27. https://doi.org/10.5539/ibr.v11n5p18

; ; (2013). The relationship between, size, growth and profitability of commercial banks. Applied Economics, 45(13), 1751-1765.

; ; (2017). Determinants driving bank performance: a comparison of two types of banks in the OIC. Pacific-Basin Financial Journal, 42, 193-203.

(2013). What determines the profitability of banks? Evidence from Spain. Accounting & Finance, 53(2), 561-586. https://doi.org/10.1111/j.1467-629X.2011.00466.x

(2002). Econometric Analysis of Cross Section and Panel Data. The MIT Press, Cambridge, Massachusetts, London, England.