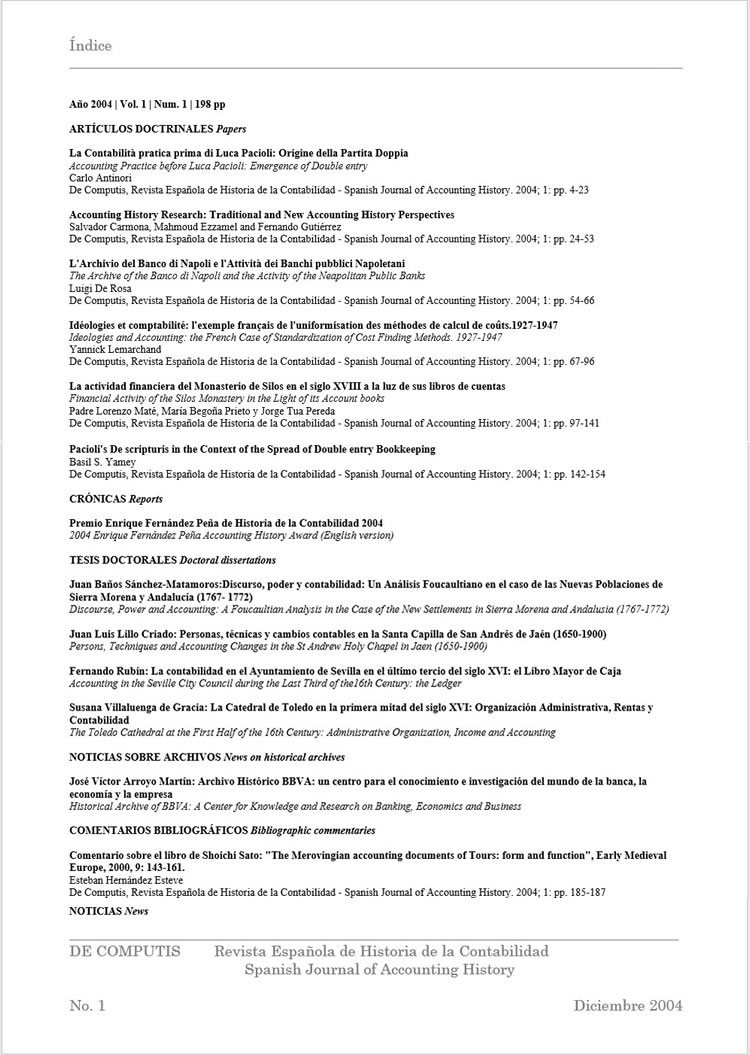

Accounting practice before Luca Pacioli

Emergence of double entry

DOI:

https://doi.org/10.26784/issn.1886-1881.v1i1.238Keywords:

Accounting, accounting, practice, history, Italy, late Middle Ages, PacioliAbstract

The paper begins with a brief review of the principal factors that limited the development of accounting records in Italy at the turn of the 13th century. These factors were the ignorance of Arabic numerals, the nonexistence of paper and the precariousness of the socio-economic conditions in many Italian regions. Despite these, the numerous monasteries found in almost all regions and the merchant enterprises in the main coastal cities, like Venice, Genoa, Pisa, etc., all kept some kind of accounting records. The hand-written Liber Abaci by Leonardo Pisano was finished in 1202 and introduced Arabic numerals in Italy; its gradual dissemination contributed, little by little, to overcome the difficulties posed by the use of Roman numerals in arithmetic calculations, above all multiplications and divisions. The first paper factory in Italy was established at the end of the 13th century in Fabriano, a city in the region of Marche. The 14th century brought increasing improvement of the socio-economic conditions in the more progressive Italian areas with the emergence of a fresh born capitalism. In this same century double entry accounting came into use, a method which became fully developed in 1430 when the first known Journals appear, i.e., the Andrea Barbarigo's Journals. Therefore, when Luca Pacioli arrived in Venice in 1465 double entry accounting had already come of age. Subsequently, the paper studies the accounting practices followed in the principal Italian regions prior to the publication of Luca Pacioli's Tractatus XI as a chapter of his Summa de Arithmetica, that is, in Venice and its territories, Milan and Lombardy, Genoa and Liguria, Emilia-Romagna and Tuscany. The particular characteristics of the various methods of accounting practised in each one of these areas are described in detail, stressing the similarities and differences among them, as well as their respective approaches toward double entry. At that point, the paper examines with special interest the statement by Federigo Melis that Tuscany was the cradle of double entry accounting. In this respect, the distinctive features of double entry as stated by Luca Pacioli are weighed in, since they are considered the essence, the true model of the method. This established, the differences between Pacioli's model and the one proposed by Melis are examined in depth. These differences are considered the result of the author¿s excessive regional patriotism, who was determined to ascribe the invention of double entry accounting to his region, Tuscany. In reality, however, it seems that this method was developed almost simultaneously in various Italian regions.

Downloads

References

Antinori, C. (1959): "Taxationes" dell'Arte dei Falegnami di Parma per il campo di Padova, Parma, La Nazionale.

Antinori, C. (2002): "I conti ai tempi dei Malatesta", SUMMA, Roma, 182.

Antinori, C. ed E. Hernández (1994): 500 anni di Partita Doppia, Roma, RIREA.

Besta, F. (1891-1910): La Ragioneria, Venezia, 1891-1910, Milano, 1932.

Bolletino Storico Piacentino (1951), Piacenza, 1° semestre.

Melis, F. (1950): Storia della Ragioneria, Bologna, Zuffi

.- (1962): Aspetti della vita economica medievale, Siena, 1962.

Pacioli, L. (1494): Summa de Arithmetica, Geometria, Proportioni et Proportionalita, Venezia, Paganino de' Paganini.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2022 Carlo Antinori

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.